you are seriously missing out) Now in this post I will be starting a new series that was previewed in my last post (see below). I thought this would be better as a standalone weekly series. In this series I will be sharing research reports from the biggest firms on Wall Street, like Goldman Sachs, Bank of America, and many others.

Our goal is to share information that is usually reserved for institutional investors and give my opinions as well.(Note that text that is italic and in parentheses is my commentary)

Table of contents:

Nomura

BofA

Goldman Sachs

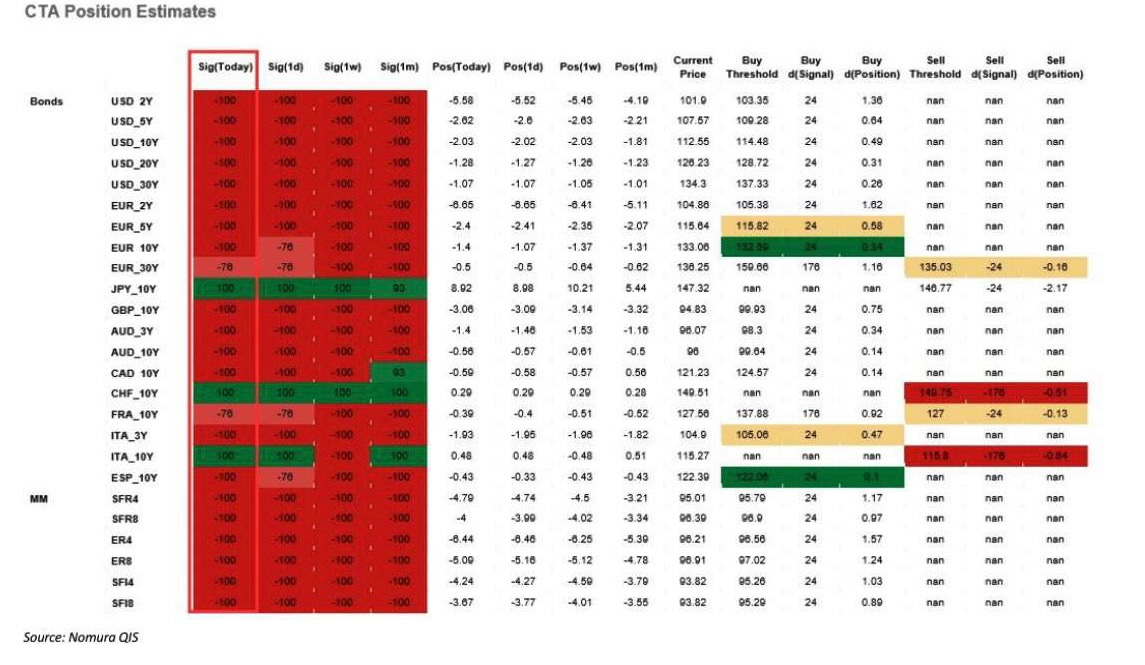

From Nomura by Mcelligott-

We are seeing resumption of client interest in 1) EM Equities Upside buying of late with funds looking for "catch-up" expressions (e.g. buyer of 50k Sep 43/45 Call Spreads day for ~$0.32, with over 90k of those spreads traded on the day; also a buyer of 30k Dec 37 Calls for $0.29 as well, with catalysts generically being "Short USD" back en vogue on "end of Fed tightening" 3.0, anticipated Chinese stim / easing, and potential for Brazilian rate cuts with EWZ Calls and Call Spreads trading)

(The inflows into EM equities does not surprise me. As investors look at forward P/E for the US equity market it makes sense investors are looking elsewhere for value. I personally would not be short the USD here I do not think inflation is done.)

Metals Upside (GDX, GLD, SLV Call Spreads in mkt of late); and from the STIRS side, we've seen 3) continued SFRM4 / U4 Upside Calls / CS trading in the market despite the recent US economic data "upside" dynamic, as "higher for longer" seemingly only increases the certainty of a harder "ultimate" recession, which alongside mounting investor confidence in continued US inflation decline is projected to merit ~150 bps of Fed cuts in 24 (Z3Z4 ~ 1.515)-while also noting that Jon Cohn on Nomura Rates Strat side 4) advocating 5s10s Steepeners or proxy trades (owning U4 or 23/U4/M5 fly)

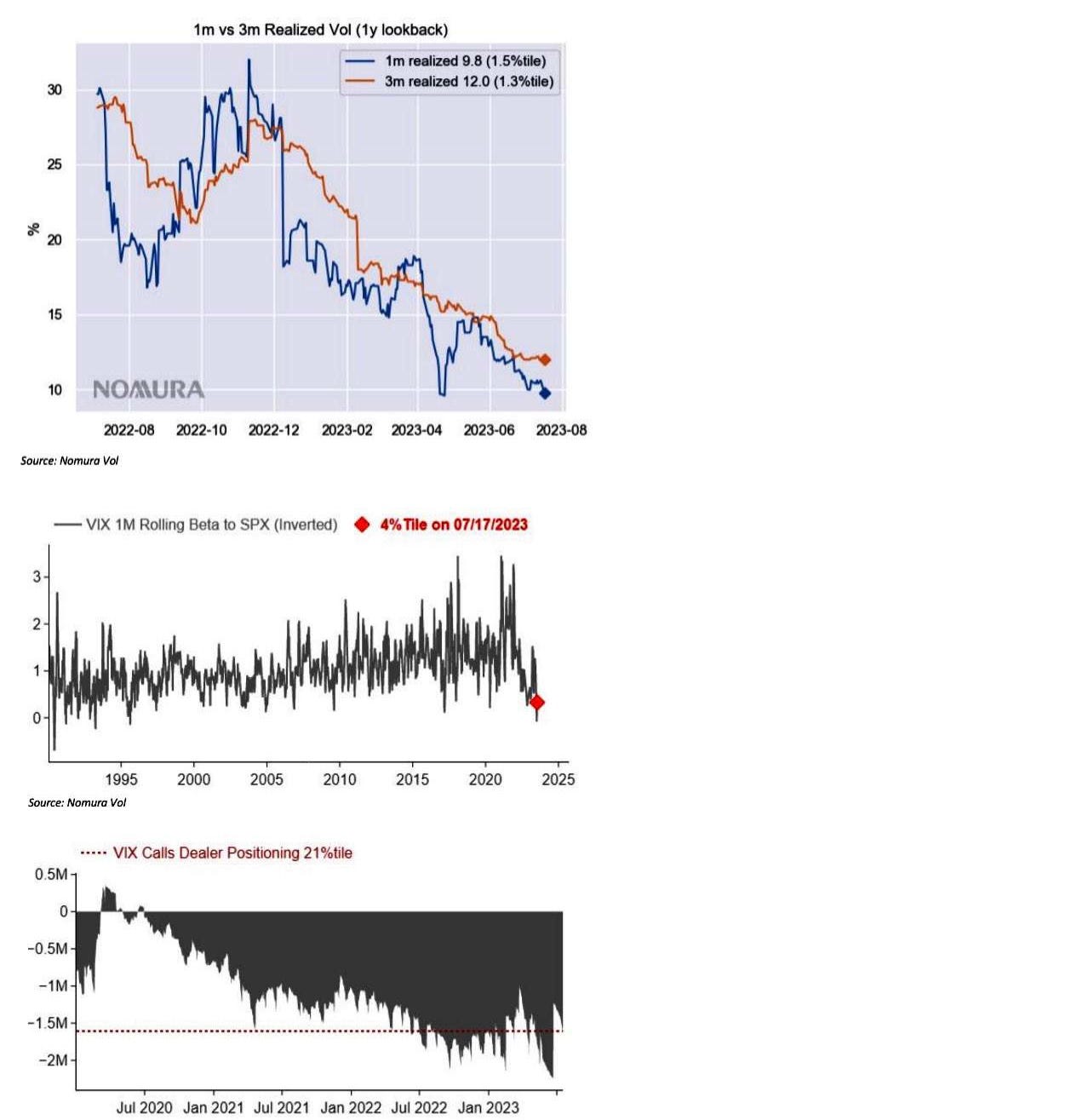

In light of so much systematic AND fundamental / asset manager Equities re-positioning having occurred in recent months, I continue to think VIX Call Spreads make sense (attractive especially with Call Skew so high), as it wouldn't take much of a Vol move to dictate a substantial Equities deleveraging blast that could really "kick-up" the illiquid VIX complex--particularly off of such a low base Vol, with SPX 1m rVol at 9.8 (1.5%ile) and 3m rVol at 12.0 (1.3%ile)

(I tend to agree with Mcelligott when it comes to VIX call spreads looking like they have a decent R:R here.[see Figure 2 & 3] The market pricing in ~150 bps of FED cuts in 2024 seems like a mistake to me with the labor market still holding up. I think it is unlikely we see ~150 bps of cuts in 2024.)

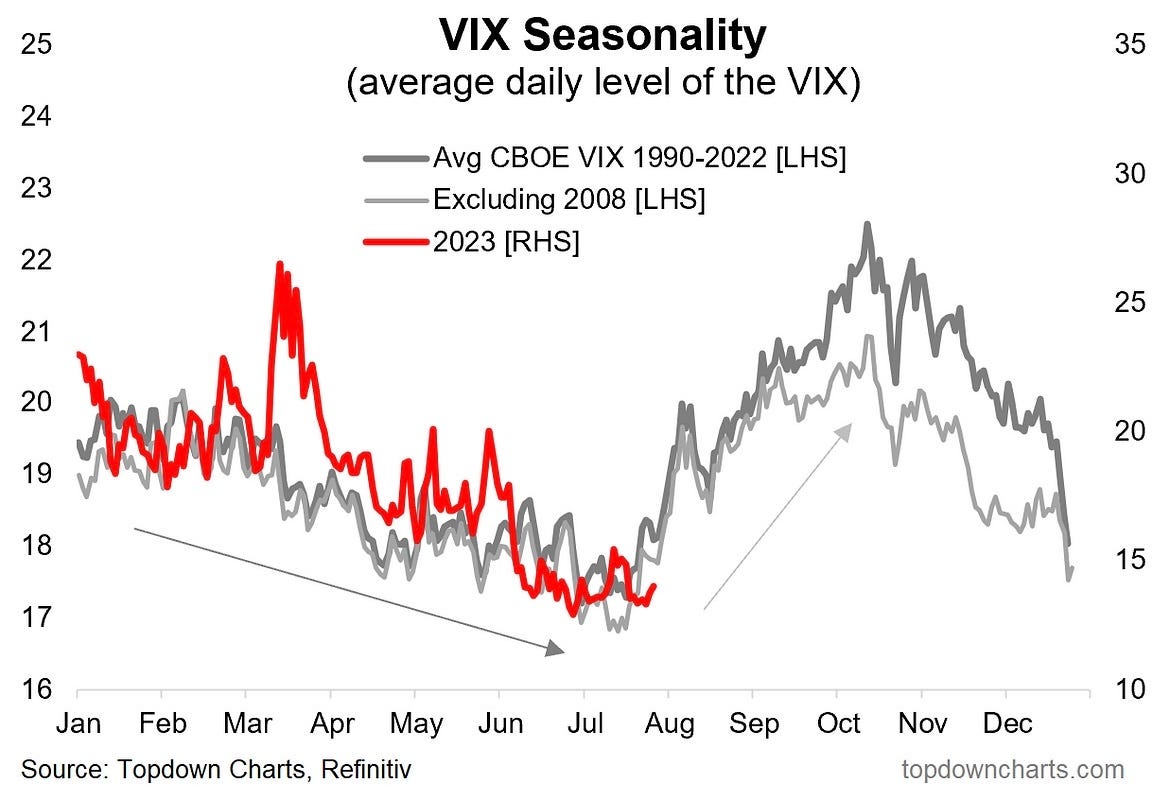

Figure 2 via topdowncharts, not in the Nomura note

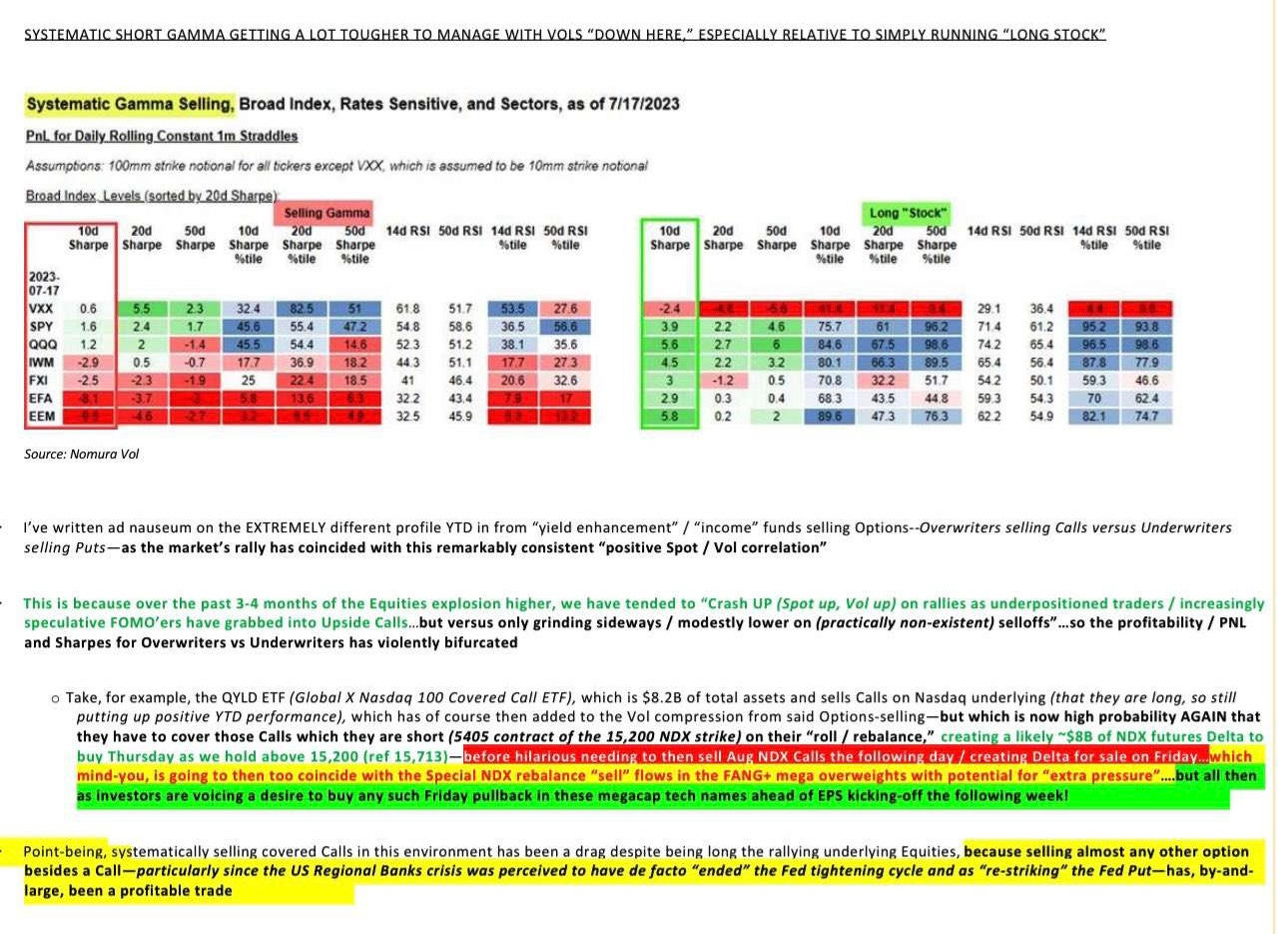

The prolific US Equities "Short Vol" environment is evolving from the past ~3 months of what was effectively "indiscriminate Vol selling"-where moving-forward, implied Vols are getting so low that you would increasingly need to shoot again realized Vol / running "short Gamma," which would mean taking-on gap risk--a much dicier proposition, especially managing around Earnings now too.

BofA Global Fund Manager Survey-

Bottom line: July BofA Global FMS sentiment remains bearish...net 60% of investors expect weaker global growth, biggest UW of commodities since May 20, FMS cash level up to 5.3% from 5. 1%, BofA Bull & Bear Indicator at low 3.5...ex. US tech, investor "fear" still greater than "greed," "Fearflation" still positive risk assets.

On Macro: most expect mild recession begins Q422/Q1'23 (note rising 19% see no recession before 2025); macro forecast of "soft landing" (68%) much higher than "hard landing" (21%); in Feb 4 out of 5 investors expected China GDP acceleration, now 1/5.

On Profits: EPS expectations least pessimistic since Feb'22...global EPS forecast to rise small 0.5% next 12 months; asked impact of Al...42% say higher profits, 1% say more jobs, 16% say higher profits & jobs, 29% say neither.

(It is very interesting that 42% of fund managers say AI will lead to higher profits. For some companies this is certainly true but most it is not.)

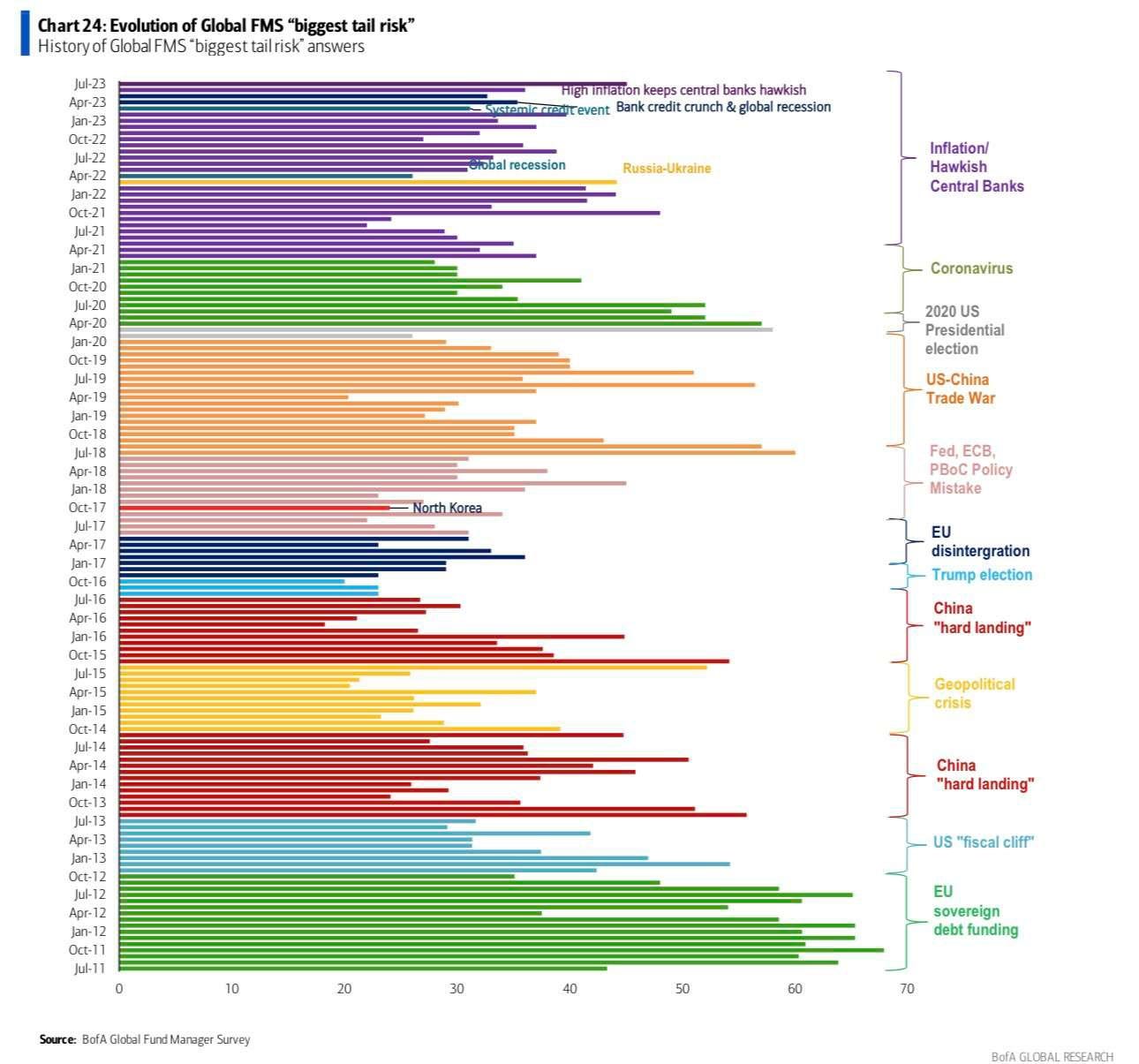

On Policy & Risks: current policy regime of "loose fiscal-tight money" most extreme since 2008; biggest "tail risk" still inflation/policy mistake (45%) then credit crunch (18% was 35% in Apr); CRE (40%) seen as most likely catalyst for "credit event”

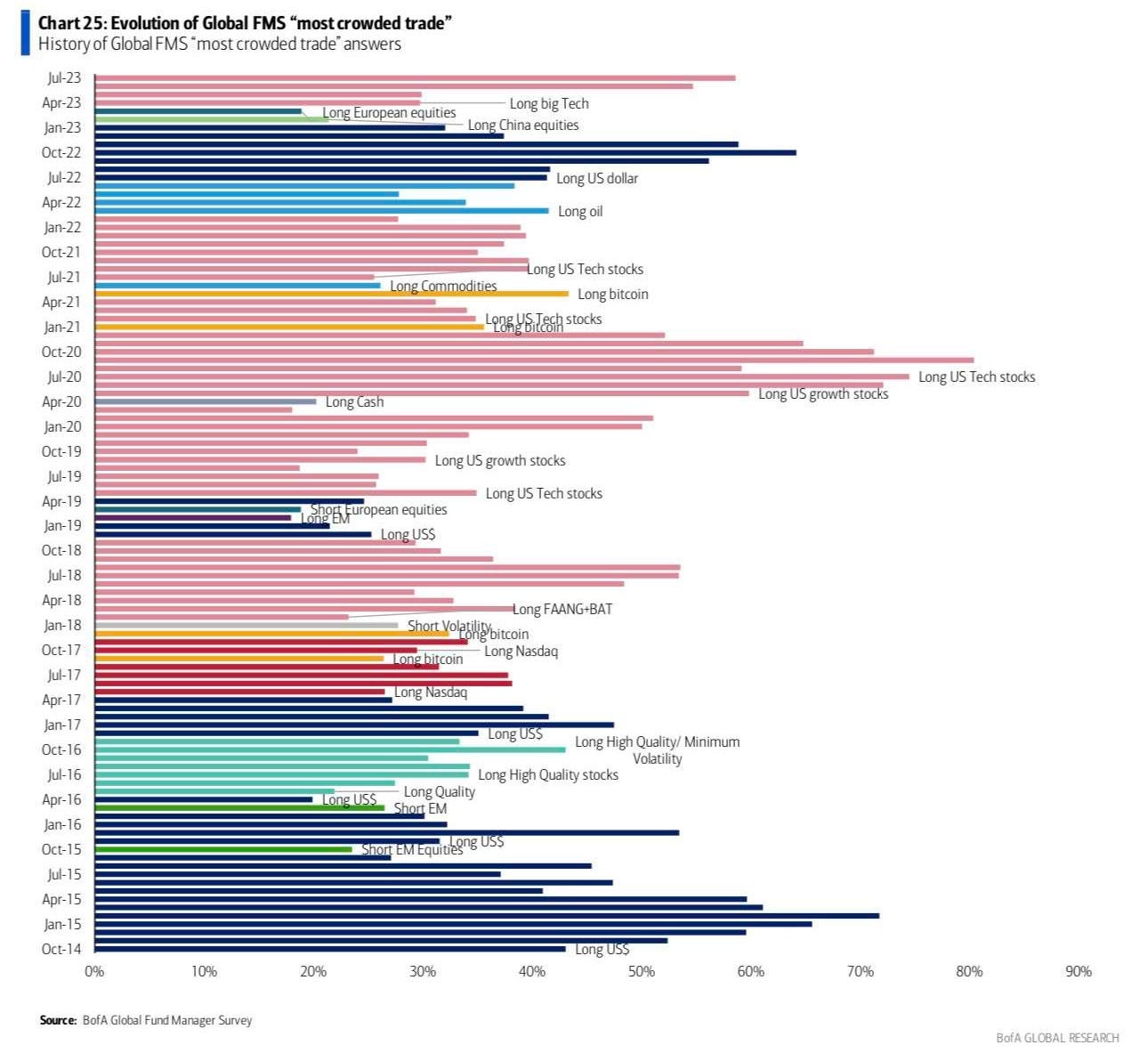

On Crowds & Contrarians: "long Big Tech" (59%) most crowded trade, then "long Japan" (14%); big short -cover in US stocks (from 44% to 10% UW); 15 UW Eurozone YTD; biggest OW global industrials since Feb'22; biggest drop in healthcare since Jan'21; contrarians would go long commodities, banks, RETs & short tech, industrials, Japan.

Goldman Sachs-

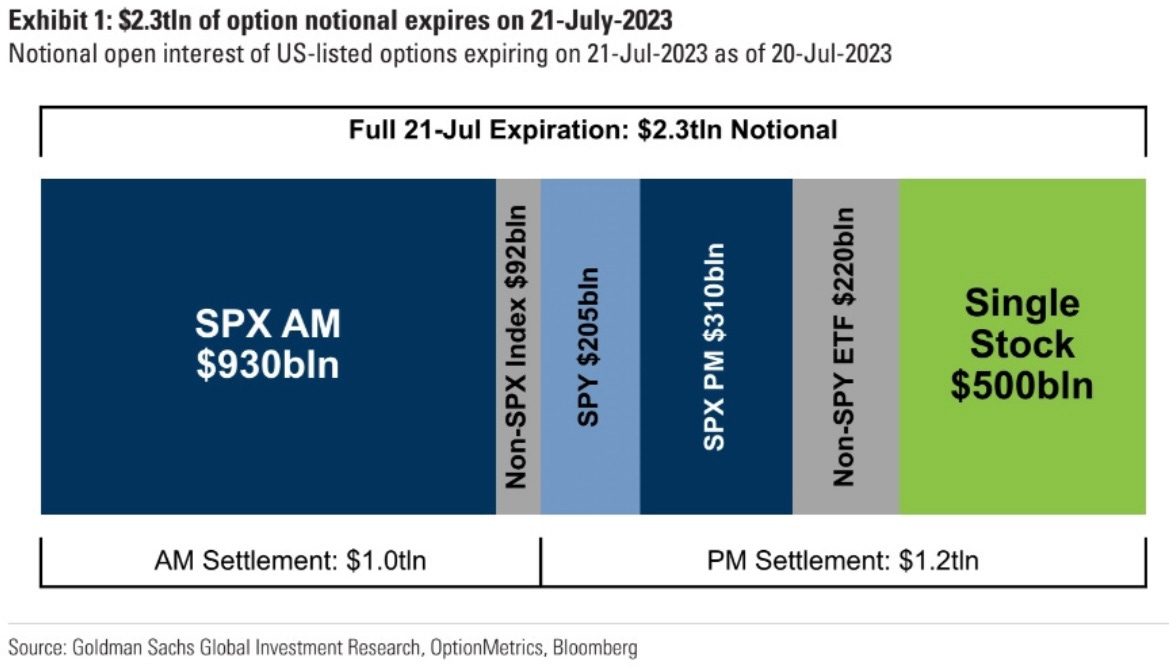

(Friday the market will see $2.3 trillion in option expiration, this is due to Opex as I am sure most of you are aware of. I expect the market to be choppy Friday.)

We believe that the higher beta (extremely volatile) names have already been covered, but capitulation in the broader universe of single stock shorts has yet to manifest.

Well that is all for now, again thank you to all of my subscribers. New and old. And a huge thank you to

DISCLAIMER: We are not Financial Advisors, and all information presented is for educational purposes ONLY. Financial markets can be extremely volatile, as such using good risk management is a must.