The Banking Blame Game #1: US Regional Banks

A new series of articles on the recent banking turmoil

This is meant to be the first of several pieces of banks both in the United States & Aboard. The working title for these articles is ‘The Banking Blame Game’. We are far from experts in these subjects but hope this informs the average trader/investor. Also if we make any mistakes in this article or future articles PLEASE let us know via the comments or our Twitter DMs. Thank you for the support!

The Recent Banking Turmoil:

Banks from small to large have been in the headlines since the beginning of this month. For good reason, with the collapse of two sizeable regional banks in the US (SVB & SNBY) to Credit Suisse (CS) needing to be bought out by UBS. The banking industry is extremely complex as we are sure everyone from Ivy league Lawyers to the average citizen would agree. Of course, this complexity is partly on purpose and the bigger reason in our view is the mixture of trying to balance industry regulations imposed by the Government with a blend of human greed, and ingenuity of humans bypassing rules or disregarding them completely.

Before we go any further we think it would be helpful to define what exactly a regional bank is. According to the Federal Reserve, a regional bank is defined as…

“The Federal Reserve defines community banking organizations as those with less than $10 billion in assets, and regional banking organizations as those with total assets between $10 billion and $100 billion.” (Source)

It is important to note this definition from the FED is extremely broad as the assets on the books to be considered a regional bank is a $90 billion gap. This is a huge number but we must also remember banks are massive with the larger banks holding 100s of billions of dollars in assets. (More on the large banks later in the piece)

In our view and many others, this banking problem is not over quite yet. In fact, the Biden Administration released a press briefing on March 30th, 2023 in-titled

Will this actually happen? Probably not, a few regional banks failing is not enough of a political burden for the US House to do anything. However, as stated above we do not think this is over. It is our view that there are three tail risk events with one or more of them likely to happen related to this banking problem. (Note these events are in no particular order of probability in our view)

More consolidation, less competition?

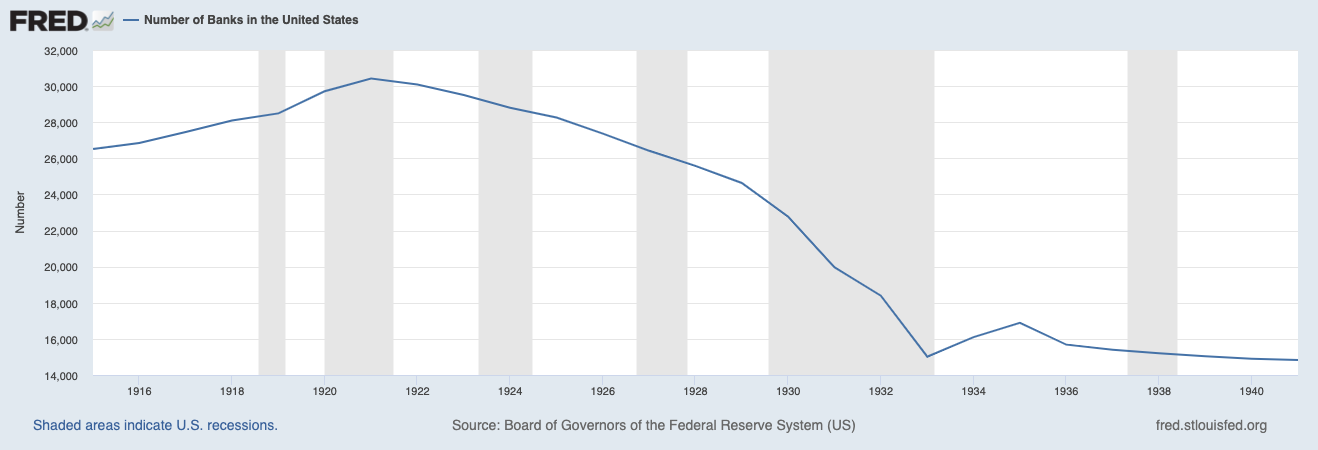

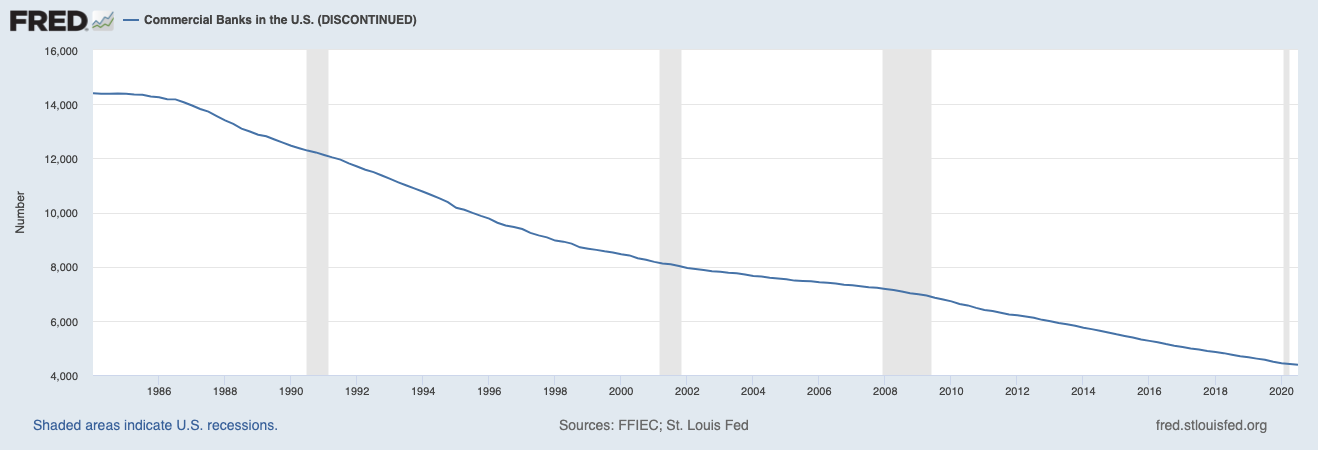

This banking problem might consolidate the banking industry even more. This has historically been what happens after a recession small and regional banks fail and the big banks buy for pennies on the dollar. Usually with bailout money from the US Government. This consolidation of banks can be seen in Figure 1 which shows the number from 1914-1945. Figure 2 picking back up in 1984 through 2020.

If this scenario plays out, it is our view that the top 25 largest banks along with other large financial institutions will take over their smaller competition.

Banks across the industry will have to “tighten their belts”, leaving regional banks holding the bag of toxic commercial real estate loans?

All of the banking industry will see a drop in profits, especially small & regional banks that are exposed to the commercial real estate (CRE) industry. In this scenario EPS across the industry will likely decrease, why you might ask. We will quote a great NBER Working Paper by Erica Xuewei Jiang, Gregor Matvos, Tomasz Piskorski & Amit Seru.

“When central banks tighten monetary policy, it can have significant negative impacts on the value of long- term assets, including government bonds and mortgages. This can create losses for banks, which engage in maturity transformation: they finance long maturity assets with short-term liabilities—deposits. As interest rates rise, the value of a bank's assets can decline, potentially leading to bank failure through two broad, but related channels. First, if a bank's liabilities exceed the value of its assets, it may become insolvent. This is particularly likely for banks which need to increase deposit rates as interest rates rise. Second, uninsured depositors may become concerned about potential losses and withdraw their funds, causing a run on the bank.” Source

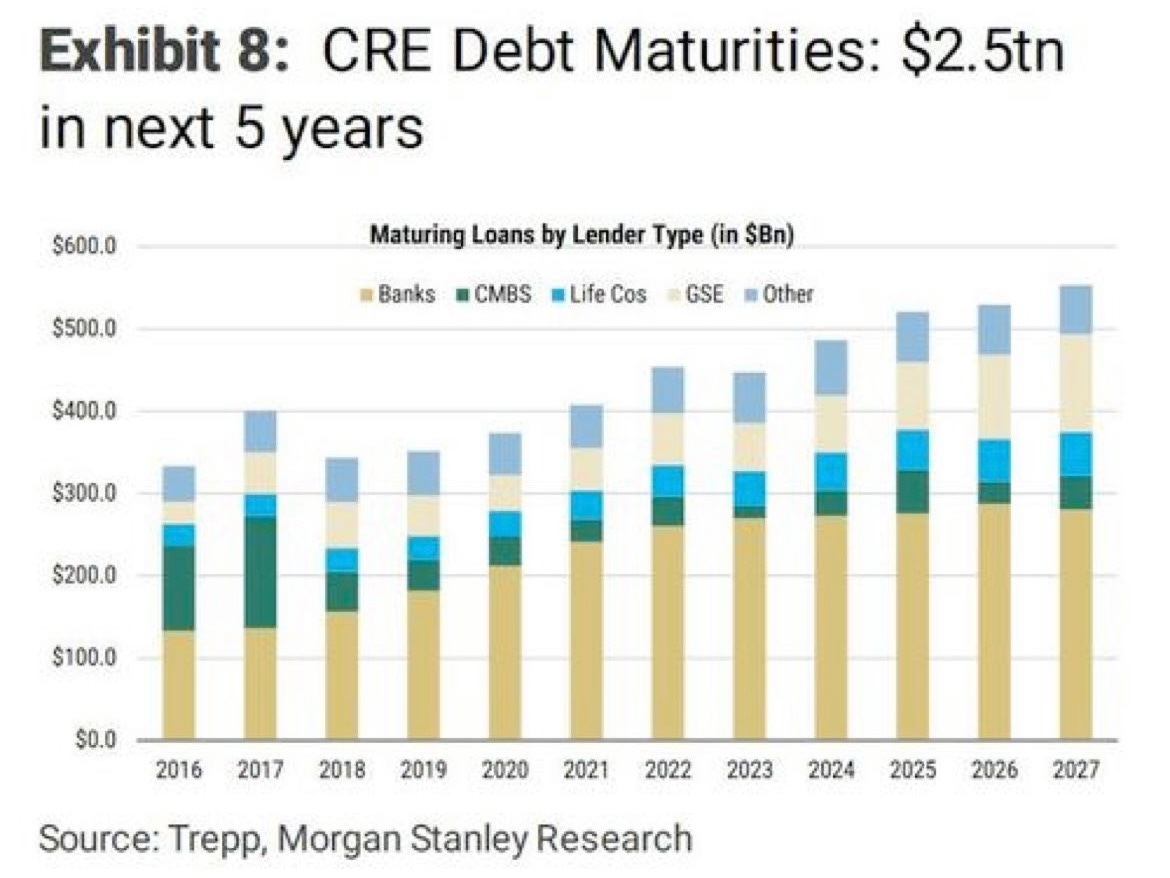

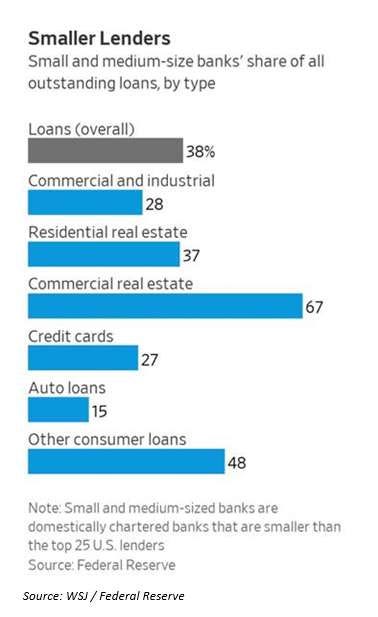

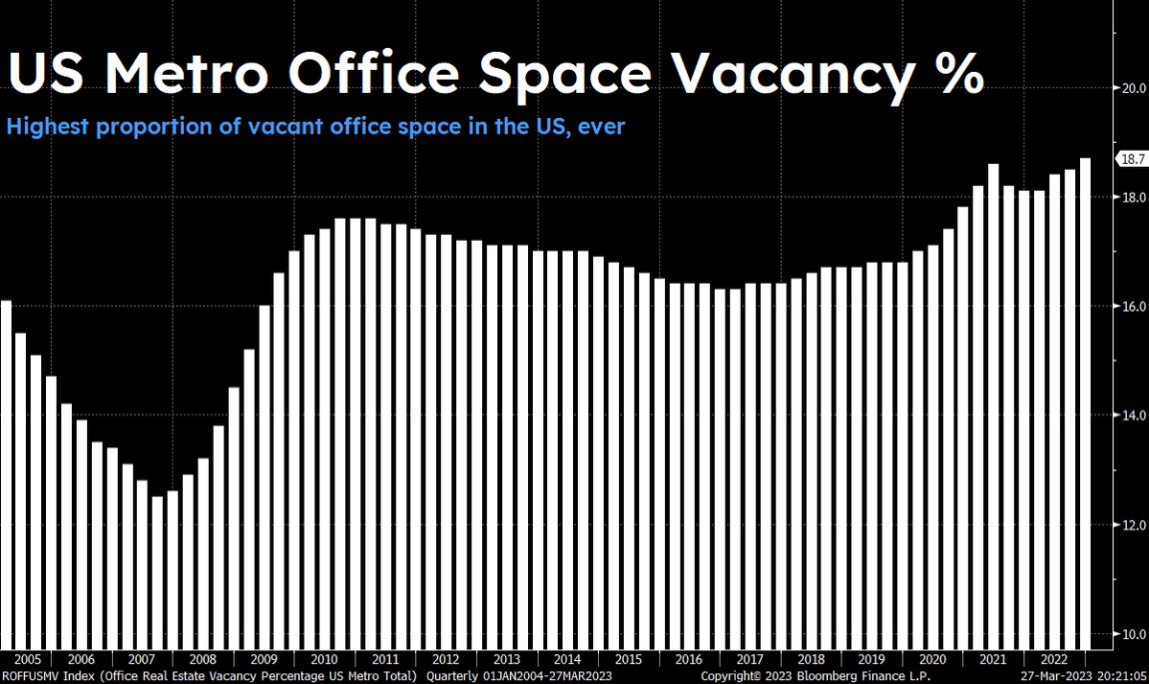

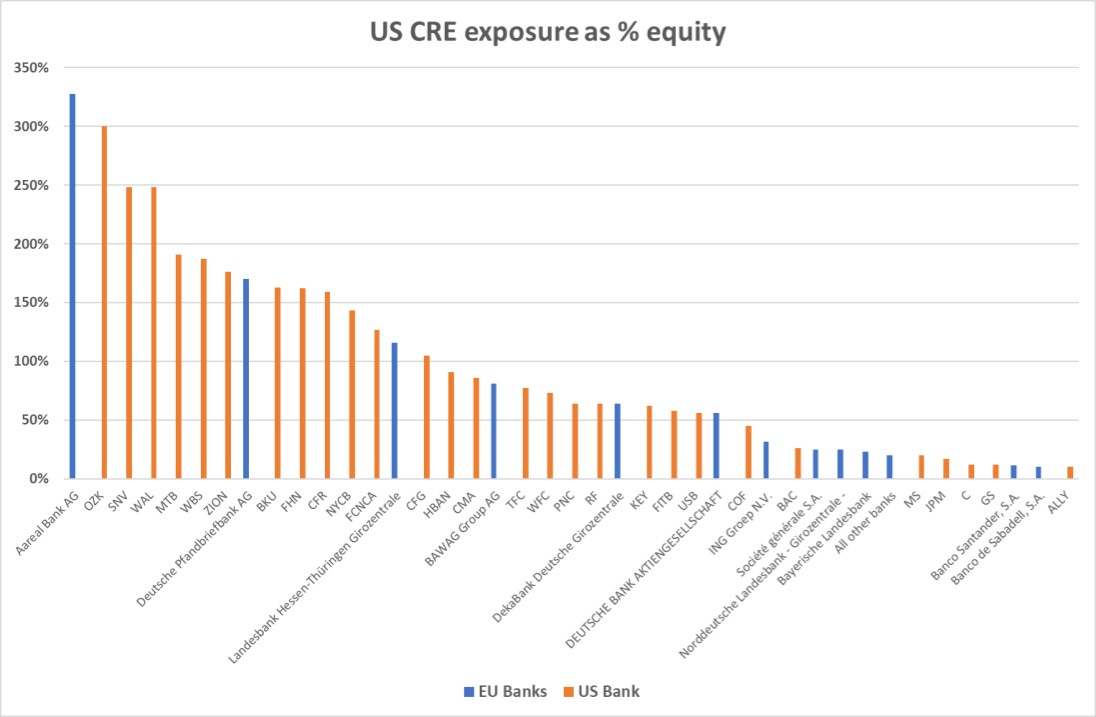

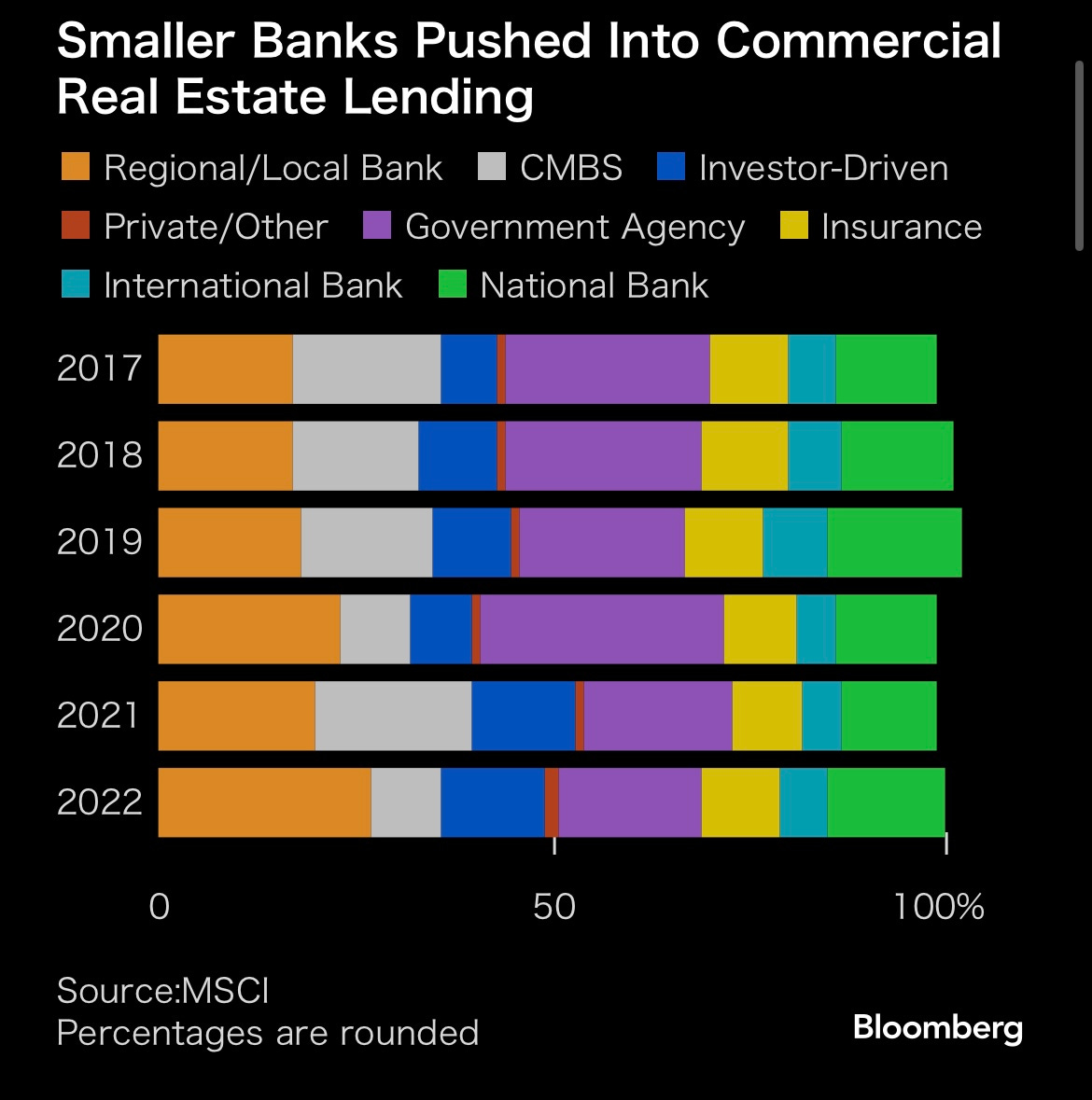

You might be wondering why we singled out smaller banks that are exposed to the CRE industry, well cracks are starting to appear in this space. A decent portion of smaller banks are not positioned to absorb these possible losses. When compared to their larger competitors. As shown in Figure 4 small banks seem to be overexposed to CRE loans. This is especially concerning when Figure 5 & Figure 6 are added to the picture. Figure 5 shows the percentage of US workers who have returned to working primarily at the office, which are often times these CRE buildings owned by small to medium size banks. Figure 6 drives the point home showing that US metro office space vacancy is at an all-time high. To add insult to injury over the next 5 years $2.5 trillion in CRE debt will mature. (Figure 3) In a low-interest rate environment, this usually would not be a problem because the banks could refinance to longer-dated debt. This is not a low-interest rate environment in-fact we are in the middle of a rate hiking cycle. So refinancing these loans would be very expensive. Finally, Figure 6 shows a list of banks that are the most exposed to CRE debt. More on possible opportunities created by this exposure in the possible trades article.

However, it is not as simple as bosses forcing their employes back into the office. As a Business Insider article explains. A few quotes from this article by Rebecca Knight that explain this issue.

“Employers across corporate America are hardening their demands for workers to return to their cubicles and rebuffing employee resistance.”

This disconnect between the employer and employee is only getting worse with HR being dragged into this spat.

“Amazon's top human-resources representative rejected an internal petition signed by roughly 30,000 employees over the company's return-to-office policy.”

This also has led increased enforcement of in-office work being tracked.

Apple is tracking employee attendance and has threatened action against staff who don't work from the office at least three days a week.

Will this increase in employers pressuring workers back into the office work? Only time will tell, but to end with a quote from the Business Insider article. *Note the original article was published by Business Insider but we linked to a Yahoo Finance mirror to avoid paywalls :)*

“But workers are ready for this battle.”

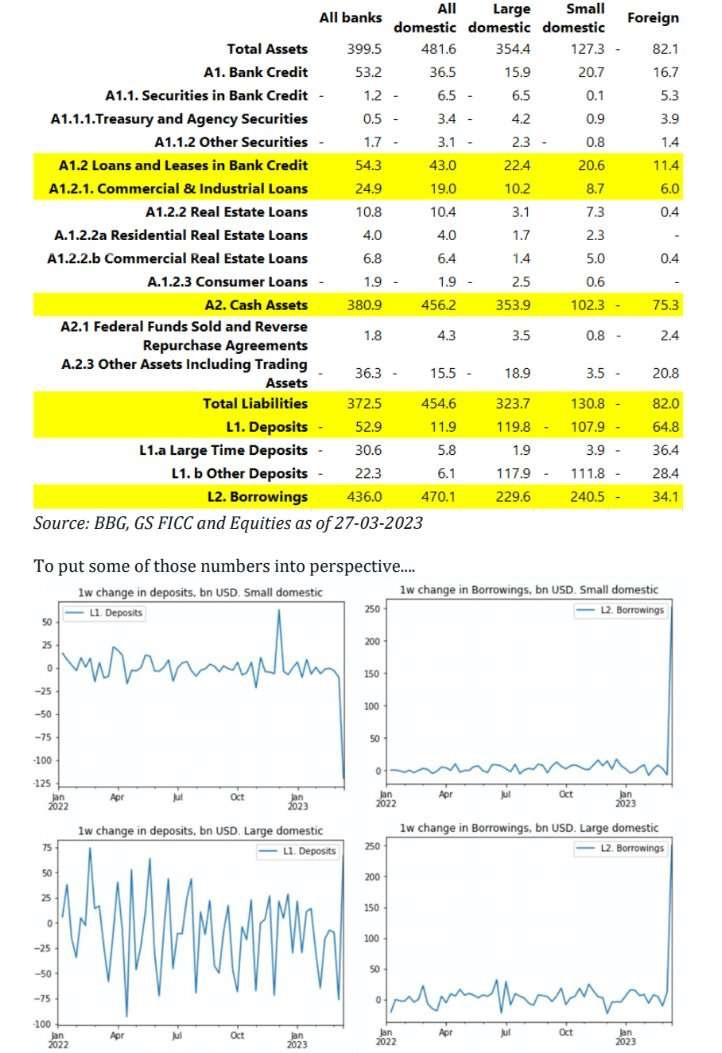

To add some more context below is some research from Goldman Sachs that breaks down the holdings and loans of both large and small banks. In Figure 8 we would like to draw your attention first to the large borrowing amount small US banks have been tapping into. (Figure 8, L2. Borrowings) The second chart in the first row of charts shows the one week change in borrowings for small banks which is a rather large increase. (Figure 9)

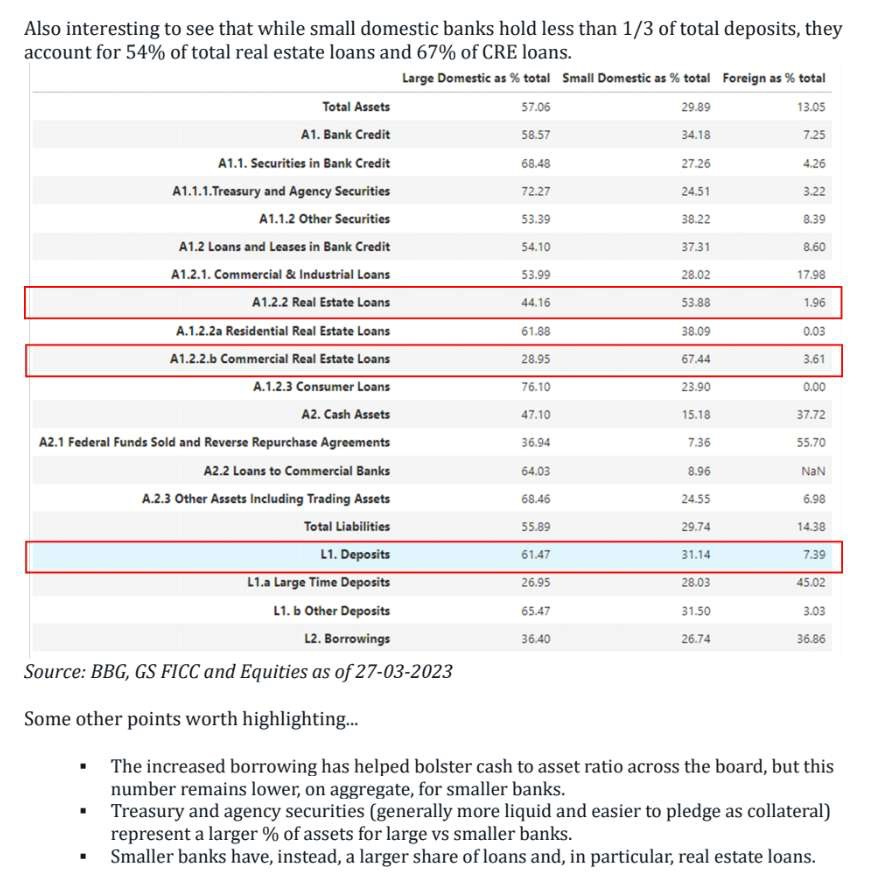

Finally, we point out the fact that small banks account for about 67% of CRE debt. In our view this scenario if it happens is likely to start unfolding later in the year. In Q2 2023 or Q3 2023 is our prediction, we believe the Effective Federal Funds Rate (EFFR) will stay elevated longer than the market is currently pricing in. This high rate environment will break the CRE “bubble”. (If you consider it a bubble we are just using this term to simplify our article)

To expand on the CRE issue even further, the Figure below shows the sizeable increase both regional/local banks have increased their CRE lending as a total percentage of the market. (Figure 10) If this scenario plays out it is likely we see more small banks fail or get bailed out by the FDIC. Or these banks will be bought by one of the large banks, which also aligns with the consolidation of the banking industry.

Return to the status-quo?

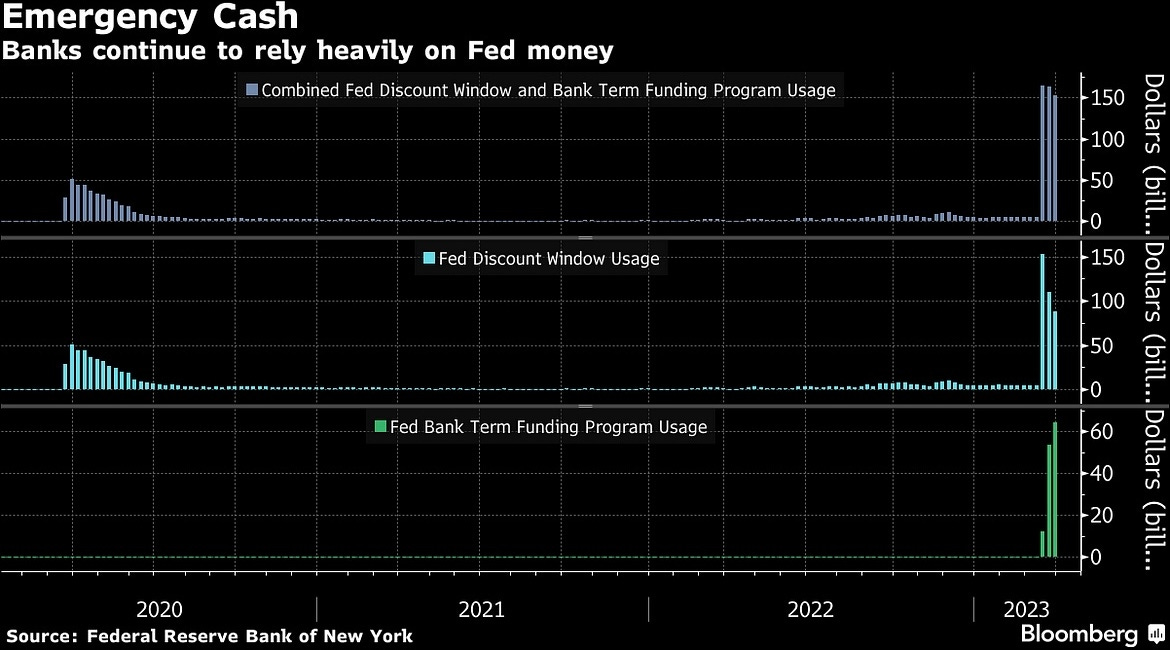

The final scenario we believe is possible is that this banking problem does not spread any wider due to the FED funding window. (Figure 11 & 12) While these FED liquidity programs certainly are not free money, due to the fact the borrowing agency has to pay the FED back at the current Overnight Borrowing Rate. This is still much more cost effective than refinancing these hundreds of millions CRE loans. These FED liquidity programs in our view allow these regional banks to keep making payments on their CRE loan obligations. Finally, if this scenario plays out we expect a few more small/regional banks to still fail. This will be the (extremely) bad firms getting punished, hopefully. Other than that in this scenario in six months this will be a distant memory.

Possible Trades?

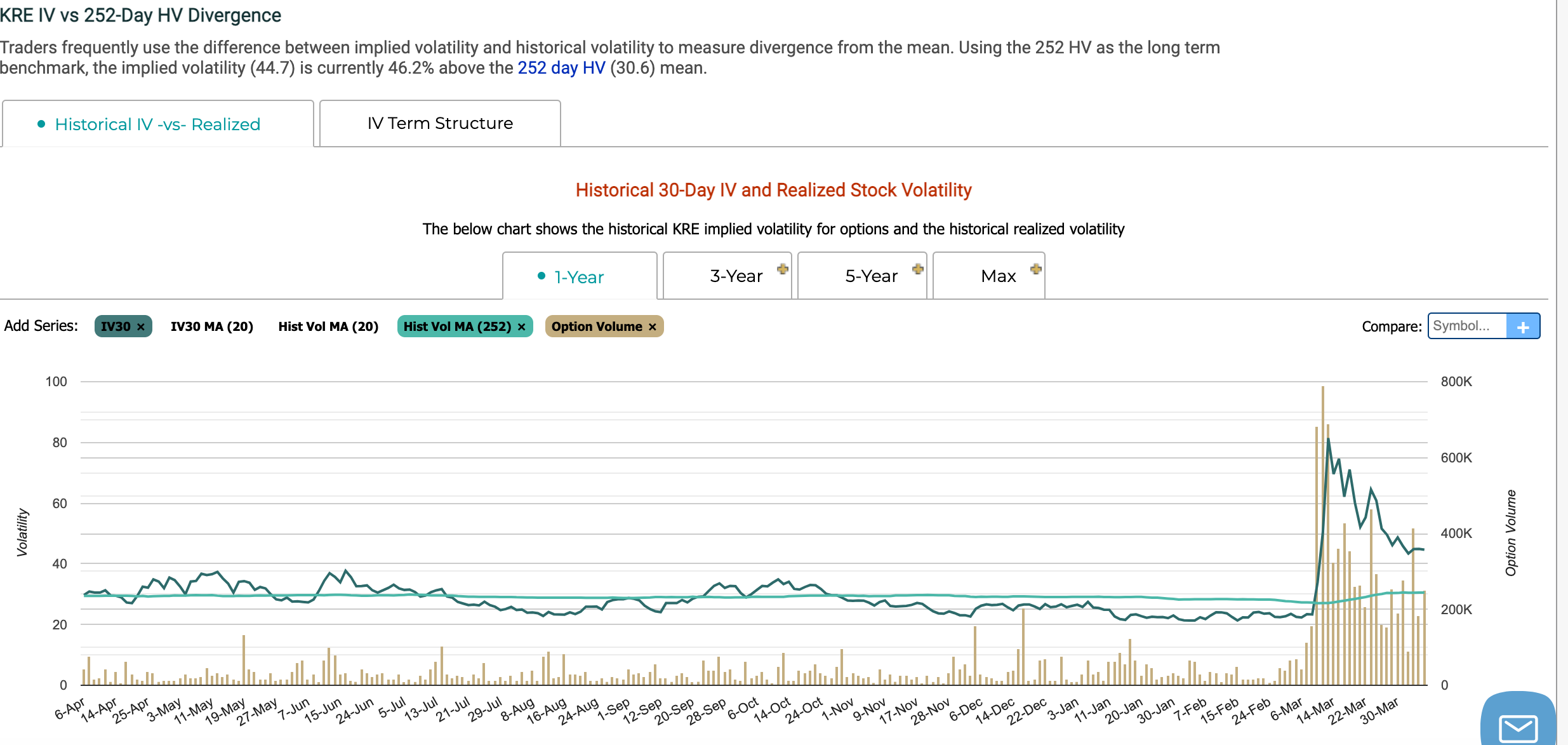

Well with this turmoil has made IV on options across the US regional banking industry extremely high as seen in Figure 13. With KRE (the US regional banking ETF) options IV being 46.2% above the 252d HV. (Figure 13) This leads up to be hesitant when looking into possible option trades. In our view this greatly reduces the R:R for these trades so we will be re-evaluating possible trades and plan on releasing a separate article soon on possible trades across the entire banking industry.

Conclusion:

In closing we at Celeritas Capital do not believe this banking turmoil will fade away totally, hence this article being the first of several related to banking industry. In the coming weeks/months we plan on writing a piece on banks that are deemed “too big to fail”, a deeper dive into CRE loans. Along with other articles, we hope you learned something from the first entry into the ‘Banking Blame Game’. Any suggestions or mistakes are always welcome in the comments!

That is all for now, thank you for reading! Any feedback positive or negative is greatly appreciated!

DISCLAIMER: We are not Financial Advisors, and all information presented is for educational purposes ONLY. Financial markets can be extremely volatile, as such using good risk management is a must.