Odfjell Technology Q2 Earnings Update

We are still rating Odfjell Technology as a strong buy. We area also adding to our shares.

Introduction:

I’m going to quickly go over the recent earnings for Odfjell Technology (OTL) and review some of the numbers from the recent earnings report. To start if you have not read our equity deep dive into OTL we recommend checking it out below.

Equity Deep Dive #1: Odfjell Technology

Hello everyone and welcome to the new subscribers! Thank you for joining and I hope this posts teaches or widens your horizons in some way. I have been working on this write on and off for a few months so some exact valuations will have changed slightly. However, I still stand by analysis. As this is my first equity write up ANY and all feedback is welc…

If you have not read the above post you will still be able to understand this post, you might just miss some context. Also after this post I plan on writing my views on the rest of the year, with trades and my macro view. Then I plan on finishing the corporate bonds primer series so be on the watch for all of that. Now lets look at Odfjell Technology Q2 earnings report.

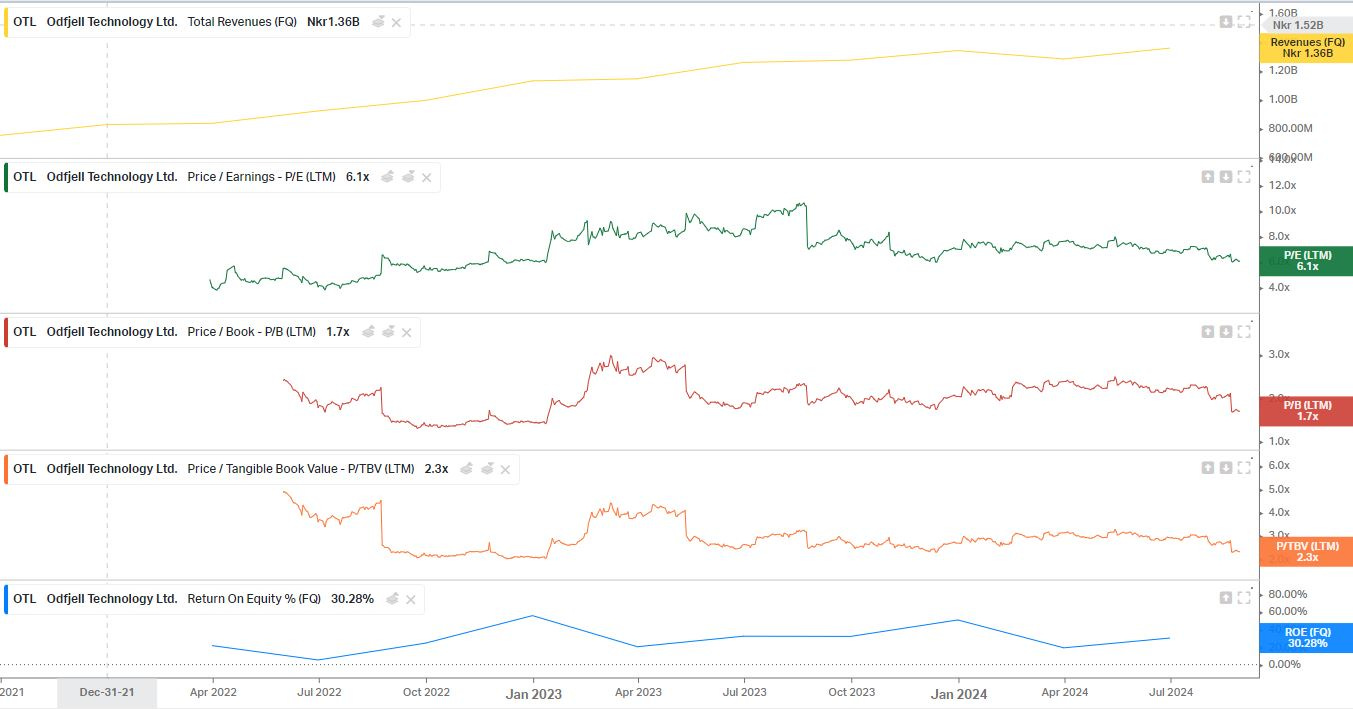

Current Value:

Below at the time of writing at 2:40am PST on August 30th is the current value. According to a number of valuations metrics, I think the most impressive metric that sticks out at me is the P/E is trading around its lowest levels since around the end of 2022. (Figure 1)

I will also include some important information on OTL again taken around the same time as the Figure 1.

Basic-

Market Cap: NOK 2,138.94M

EV: NOK 2,849.34M

Shares Out: 39.46M

Revenue: NOK 5,259M

Employees 2,480

Margins-

EBITDA: 14.44%

Operating: 9.52%

Pre-Tax: 7.58%

Net: 6.87%

FCF: 7.57%

Q2 Earnings:

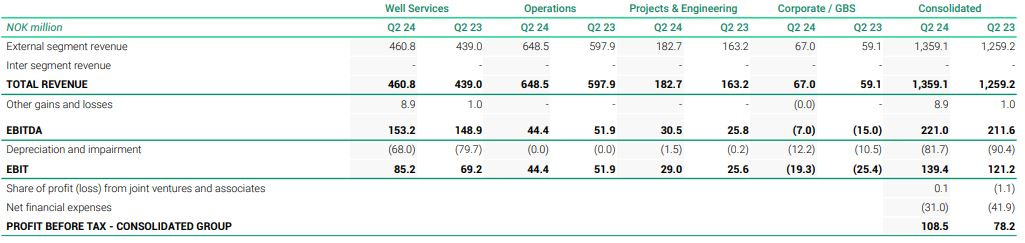

OTL double beat their street expectations for EPS and revenue. With coming in at 2.18 with an estimate of 1.85 or a beat of 17.84%. As for revenue it was still a beat but not as big of one, revenue came in at NOK 1.359B with expectations set at NOK 1.288 or a beat of 5.56%.

Above in Figure 2 we can see which segments of Odfjell Technology grew the most in the past quarter. First lets start with operations,

Operations Performance:

Q2 2024 revenue increased to NOK 648.5 million, compared to NOK 598 million in Q2 2023.

EBITDA fell to NOK 44 million from NOK 52 million in Q2 2023.

The EBITDA margin decreased to 7% from 9% in Q2 2023.

Challenges:

Lower EBITDA was due to additional costs from crew transportation delays, higher sick leave, and reduced bonus earnings.

“This is mainly explained by increase in activity, compared to Q2 2023, related to management of the jack-up rig Linus for SFL Corporation Ltd and an increasing demand for construction and inspection services through Rig Inspection Services.”-OTL Q2 earnings report.

Year-to-Date YTD Performance:

YTD 2024 revenue rose to NOK 1,238 million, compared to NOK 1,156 million in YTD 2023.YTD EBITDA decreased to NOK 57 million (from NOK 86 million), with a reduced margin of 5% (from 7%).

Well Services Performance:

Performance:

Q2 2024 revenue increased to NOK 461 million, up from NOK 439 million in Q2 2023.

EBITDA grew to NOK 153 million from NOK 149 million in Q2 2023.

The EBITDA margin slightly decreased to 33% (from 34% in Q2 2023).

Drivers of Growth:

Increased activity in Namibia, Kuwait, and Saudi Arabia more than offset the non-renewal of a high-margin contract in Norway and the winding down of a UK operation.

YTD Performance:

YTD 2024 revenue was NOK 928 million, up from NOK 832 million in YTD 2023. YTD EBITDA rose to NOK 328 million (from NOK 285 million), with an improved margin of 35% (up from 34%).

Projects & Engineering:

Performance:

Q2 2024 revenue grew to NOK 183 million, up from NOK 163 million in Q2 2023.EBITDA increased to NOK 30 million, compared to NOK 26 million in Q2 2023. The EBITDA margin rose to 17% from 16% in Q2 2023.

Growth Factors:

High activity in Bergen, Stavanger, and the UK, driven by Special Purpose Survey (SPS) activities and modification work on the Heidrun B Floating Storage Unit.

YTD Performance:

YTD 2024 revenue was NOK 345 million, up from NOK 303 million in YTD 2023. YTD EBITDA was NOK 55 million, slightly higher than NOK 54 million in YTD 2023, with a margin of 16% (down from 18% due to the impact of high-margin activities in Q1 2023).

Acquisitions:

OTL acquired 100% of McGarian TDC Ltd. in May 2024. McGarian TDC Ltd. specializes in designing whipstocks, casing and packer milling, and fishing and remedial products. This acquisition supports Odfjell Technology's strategy to expand its service portfolio and strengthen its capabilities in the Slot Recovery and Plug and Abandonment sectors. The deal includes a base payment of GBP 3 million, with additional earn-outs based on commercial success and product development targets over the next three years.

I am interested in how this new acquisition will help OTL but the company only spent 3 million GBP. Hopefully this can help with some of the lacking EBITDA.

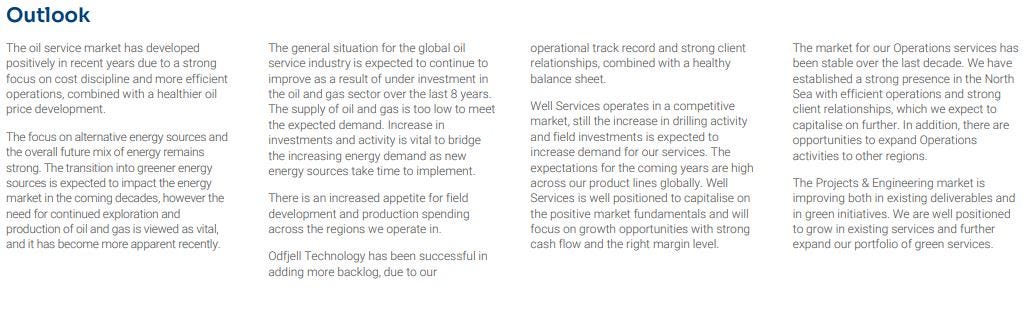

Outlook:

Risks:

Conclusion:

I want to comment on the sideways action we have been seeing on OTL. The stock is actually down around 8.5% since my first published report on OTL. For me this is a multi year investment. Below is a chart showing the current ranges as I see them. I’m a buyer through bottom channel but hopefully it bounces. (Figure 5) Finally the next post I’m working on is my outlook for the rest of the year. It will have trades and my macro takes, so don’t miss that!

If you feel like you want to review the report I will link the website where you can download your own copy of the report from OTL and review it. (Click review it) Thank you for reading!

DISCLAIMER: We are not Financial Advisors, and all information presented is for educational purposes ONLY. Financial markets can be highly volatile, so good risk management is a must.