Markets Malarkey 2/13-2/17

Rundown from last week:

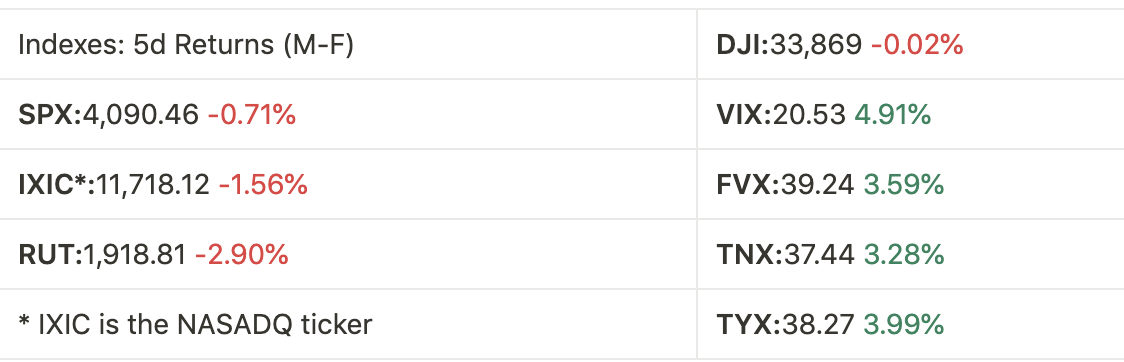

All of the major US equity indexes ended the trading week in the red. With best performance going to DJI (-0.02%) & the worst being RUT (-2.90%) as shown in the table below. We believe this small sea of red in the indexes is likely due to a technical pull back. Along with the upcoming wave of economic data this coming week. In opposition to the US equity market ending the week down, the US treasury yields increasing all at least 3% by the end of week. With the TYX leading the charge followed closely by FVX. (Note to get the yield for FVX,TNX,TYX simply move the . one place to left i.e. TNX 37.44 = 3.744%) The final thing we would like to highlight is the VIX rising just under 5% (4.91%) this week. We believe having the VIX around the low 20s is a healthy place.

Preview for this week 2/13-2/17:

Economic Data & Earnings

As mentioned in the previous section there is a lot economic data being released this week. Including on Tuesday 2/14 CPI data (-0.1% predict MoM) and Wednesday 2/15 the Empire Manufacturing along with Retail Sales data. However perhaps the most important day of the week is Thursday 2/16 with most important for the Marco outlook being the Initial Jobless Claims. (More on this in the Marco Outlook section) But it is not only the Initial Jobless on the 16th that the market will likely be watching, these other data releases include Building Permits, PPI & Continuing Jobless Claims. Overall we expect this week to be semi volatile, which opens up the opportunity for countless trades. However of course with this volatility comes risk for both long and short positions in equities. We are going into this week all cash and recommend anyone with positions look at possibly hedging going into these economic data releases.

There is also a large amount of earnings reports releasing this week. We would first like to highlight KO releasing their ER Tuesday BMO. Also on Tuesday we have DVN, ABNB & UPST all AH. On Wednesday BMO we have RBLX & BIIB, with SHOP, TWLO, ROKU & MRO AH Wednesday Finally we will be watching DE (Deere & Co) which will be reporting Friday BMO.

Fixed Income

We believe that yields will likely see a slight pullback on Monday. However the rest of the week we think the previously mentioned economic data wave will decide how yields react. We included some basic charts for the FVX, TNX, & TYX. For the bull case look for a break of the trendlines (the yellow lines). For the bear case we would like to point out the white lines on Figure 3-Figure 5, this is the 200d weighted moving average (WMA). The 200d WMA has shown to be a strong support for all US treasuries for past few weeks. So in a bear case for treasuries we see the yields heading towards their respective 200d WMA. With the red lines on Figure 3-Figure 5 being the 200d simple moving average (SMA) also looking like a strong support.

Marco Overview:

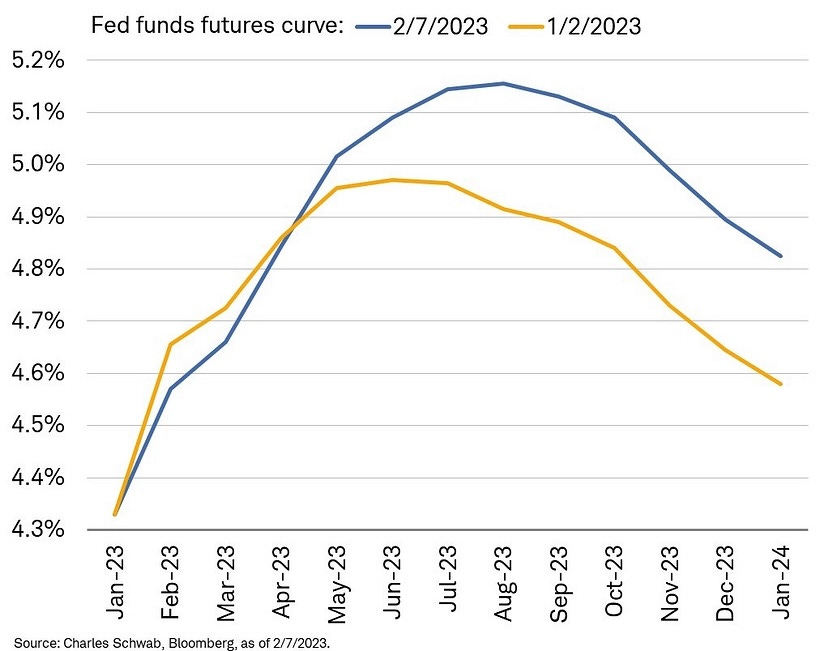

The FED has made it clear that it cooling down the labor market is key to bringing down inflation to its stated goal of 2% inflation. “We will need further rate increases, still have not reached sufficiently restrictive level, disinflation has begun but has a long way to go, strong jobs report shows why this will be a long process, the reality is that we're going to react to the data, would certainly raise rates more if data were to come in stronger, will certainly take until next year to get down close to 2%” -Jerome Powell 2/6. After a Q&A on 2/6 where Jerome Powell mostly restated his what he has been saying, which is summed up in the quote above. The markets seemed to listen as the next day the Fed funds future curve priced in the FED holding at 5% until Dec-2023. (As seen in Figure 6)

The labor markets strength appears to still be holding strong in our view. Even with last Initial Jobless Claims rising for the first time in six weeks last release, this is more than likely due to termination of seasonal holiday jobs. Even with the increase of jobless claims last report the 4 week moving average has dropped to the lows of April 2022. (Figure 7)

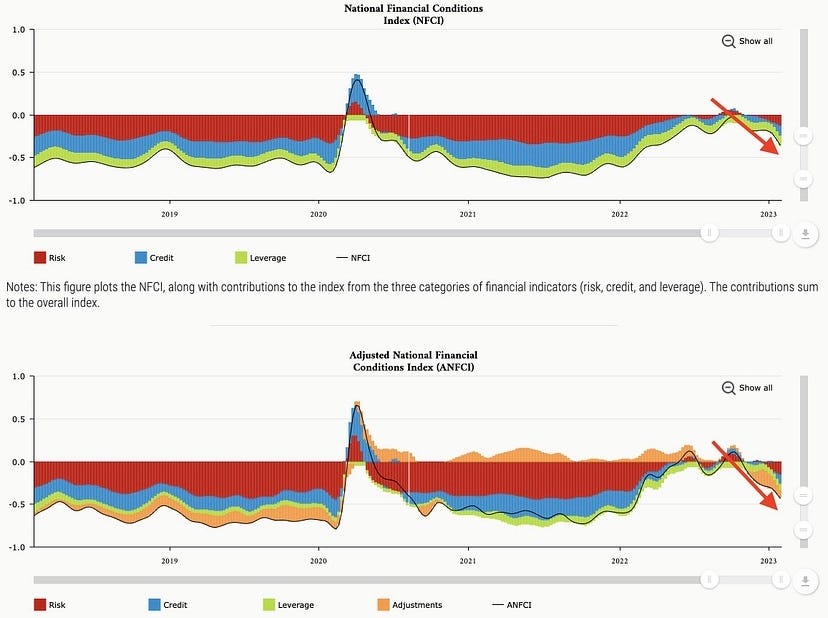

It seems almost certain at this point the markets and economy are finally listening to the FED and tightening financial conditions, as seen in Figure 8. We expect this tightening to continue throughout the rest of the month. However even with this tightening consumers keep increasing their credit amount. As seen in Figure 9.

*THIS IS NOT INVESTMENT ADVICE*