Markets Malarkey 2/20-2/26

Weekly Markets Update

Rundown from last week:

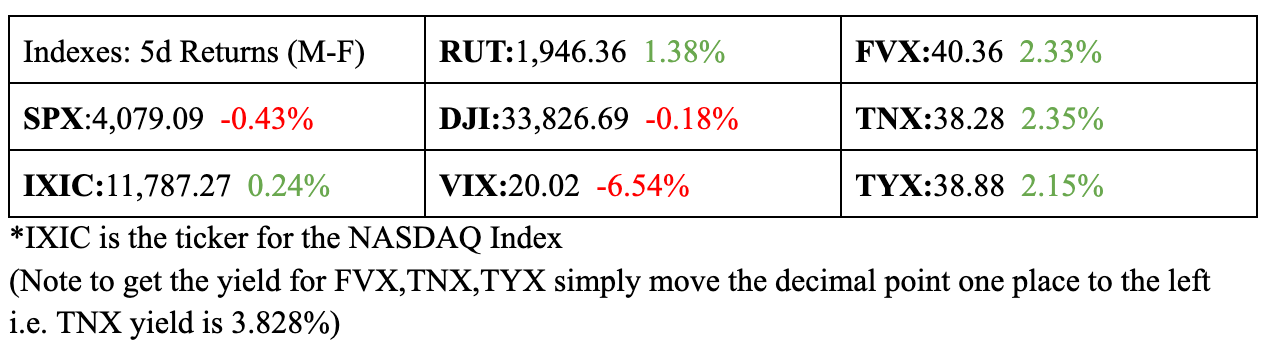

First we will take a look at the major US Index returns from the previous trading week. Again we have a mixed bag with half of the major equity indexes ending the week green (RUT & IXIC). With SPX and DJI ending the trading week slightly down. US Treasuries ended the trading week up at least 2% with the TNX leading the charge with a 2.35% gain this week. As a quick note we would like to draw attention to the VIX. Do not be fooled by -6.54% the VIX is very much active. The price and upcoming events are much more important to the VIX (more on this later).

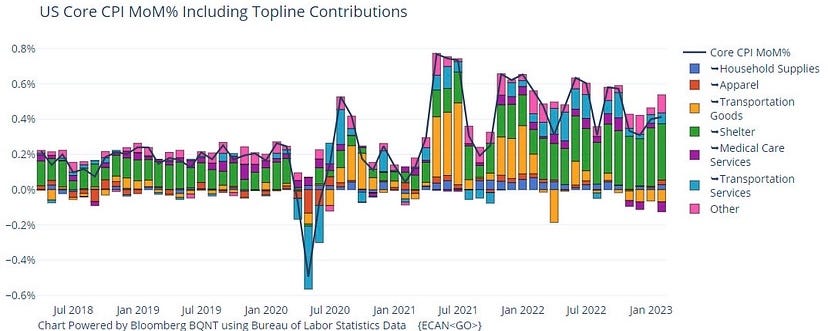

Well after a busy week of economic data being released including CPI & PPI prints. Among others including the Jobless Claims (and many more) & some jawboning by FED members. We must admit we got the CPI print wrong with us expecting a colder print. However in January 2023 US CPI MoM increased 0.5% vs the 0.1% increase of December 2022. With shelter making up the largest increase in the CPI Core data as shown in Figure 2.

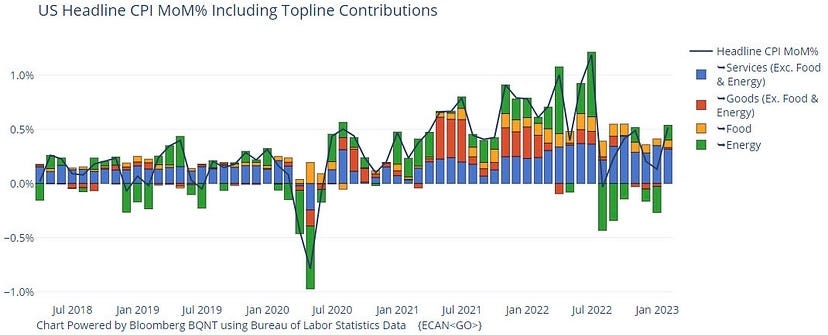

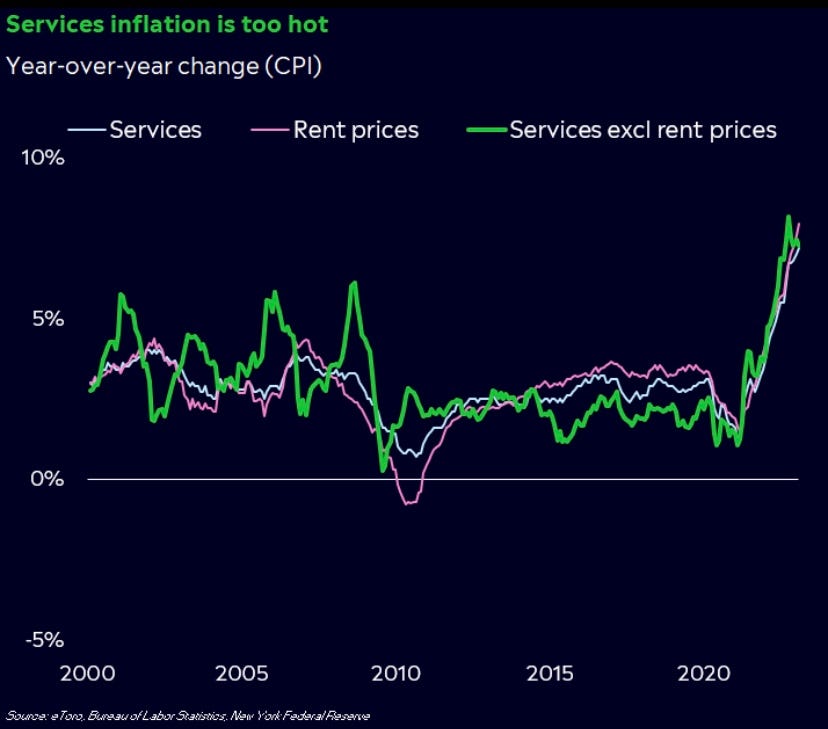

Next we would like to take a look at Headline CPI data for January 2023. With the largest contributor being services with energy increasing as well. (Figure 3) In a similar vein we would like to highlight the fact that services even with rent, food and energy excluded still looks quite high. (Figure 4) In our view this shows that consumers are still spending even with elevated inflation. These recent data releases particularly the US Headline CPI, highlights that in our view the FED has a lot of work to get inflation back down. (More on this in a future piece)

Preview for this week 2/20-2/26:

Earning Reports

Another week more earnings, to start the week on Tuesday the 21st (US equity markets are closed on Monday the 20th due Presidents Day) BMO we have WMT & HD both of which should offer interesting views on consumer spending. Also on the 21st AH we have COIN & TOL among others. We are interested in COIN because in our view it is extremely overvalued and we expect a price correction in COIN by the end of Q3 at the latest. TOL on the other hand is a much more solid business, the future guidance will likely be the important information from earnings release. As it will give investors a view on how homebuilders expect the fiscal year to go. On Wednesday the 22nd we have BIDU reporting BMO, but the real fireworks are scheduled AH Wednesday. Including NVDA, LCID, ETSY & BROS. Finally on Thursday the 23rd BMO we reports from BABA, MRNA & W, NKLA. In our view both W and NKLA are overvalued by an insulting amount especially W. (W as of Q3 2022 had a little over $6 billion in liabilities and around $3.5 billion in assets on their books)

Fixed Income

This week we will be keeping a close eye on the US Treasury yields, as we mentioned in our bull case from last week’s newsletter the 5Y yield (FVX), 10Y yield (TNX) & 30Y yield all broke their respective trendline. With the 5Y and 10Y still holding above their trendlines as shown in Figure 6 & 7. We expect that the old resistance trendline on FVX to act as new support area.

The 10Y yield is in an interesting place from a TA standpoint. If equities rally during this week it is possible to see TNX head downwards towards the first gap down (shown as a red shaded in Figure 7). However if the equity market falls or trades choppy this week we expect TNX to also have it’s old resistance trendline turn into a support as yields keep rising.

The 30Y (TYX) broke it’s trendline but then was rejected again. This week based on our TA we expect a small pullback on TYX.

VIX

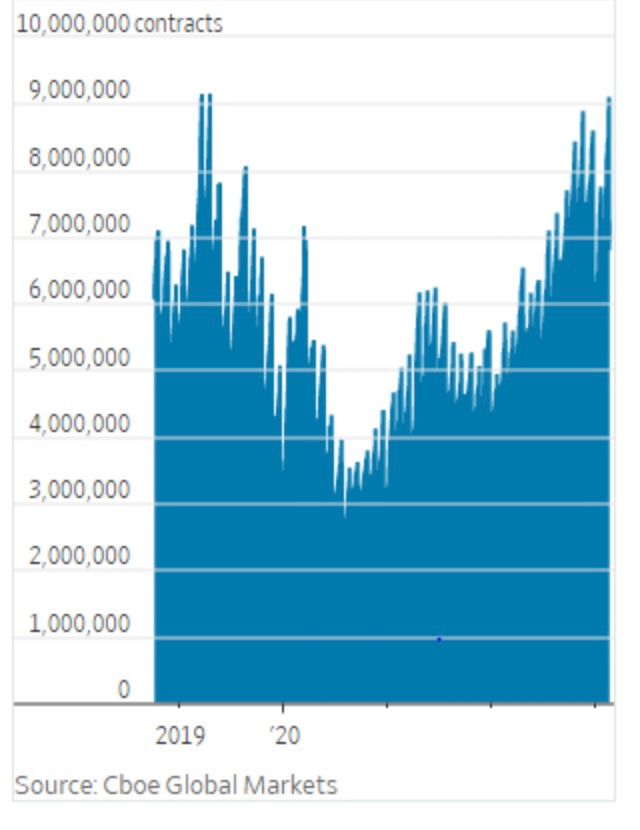

The last thing we would like to highlight is the VIX and volatility as a whole. For the past few months the VIX has been relatively stable, however we believe this might be coming to an end soon. Here is why, first it does not have anything to do with 0TDE SPX options. Instead in our view market participants are finally realizing that the soft landing is getting less and less likely. For example look at Figure 10 which shows the total number of VIX calls being bought. Market participants clearly are seeking some exposure to a market downturn or a Black Swan Event.

We usually are in the camp that trying to do any TA on VIX is mostly useless. That being said we believe Figure 11 shows an interesting trend of rejection to the upside. This rejection is point is also the start of a gap up on the daily chart. If the VIX is able to breakout out of that rejection zone we predict a gap up towards 25 for the VIX.

Possible Trade Setups:

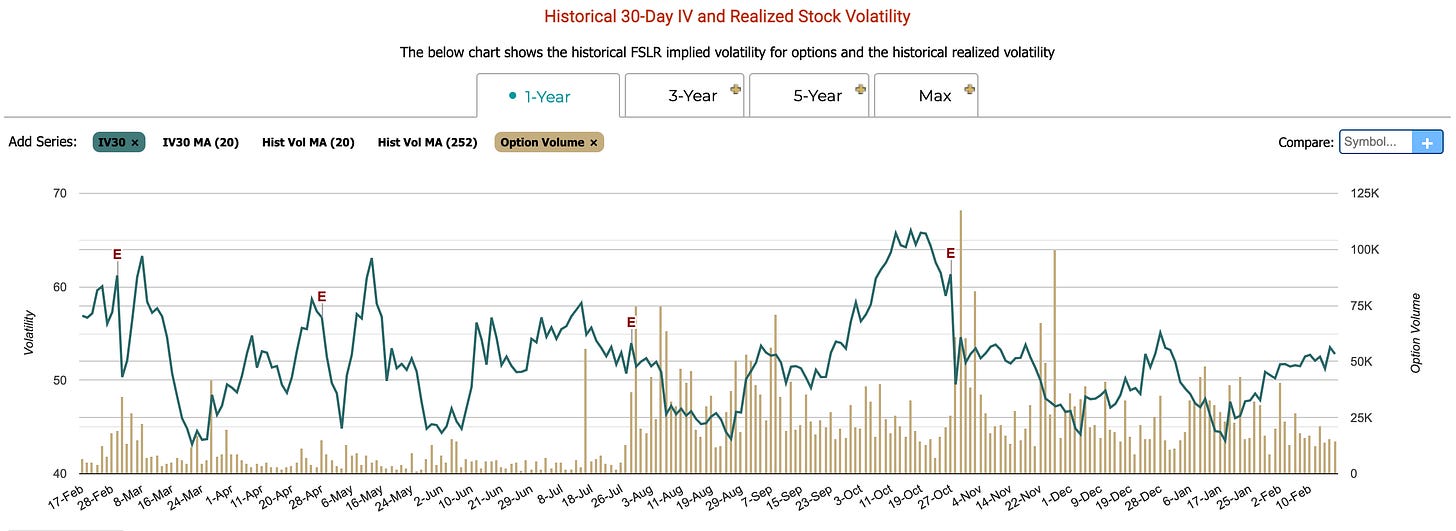

Buy FSLR calls, reasoning cheap IV on options compared to the last lead up to the previous earnings release (ER). FSLR releases their Q4 2022 ER on Feb. 28th.

Figure 12 via Market Chameleon Short TLT if 30Y yield retests trendline (Figure 8), safest way to short is via puts.

EBAY: If you are bullish on the US consumer buy calls ahead of EBAY’s earnings (2/22 AH) On the opposite side puts have a large inflow and the EPS estimate is the highest since Q4 2021.

Buy UVIX calls, this is a very risky trade so tread carefully. In our view ATM calls with an expiration in the next few weeks may be able to capture decent profit.

Marco Overview & Our View:

Central Banks

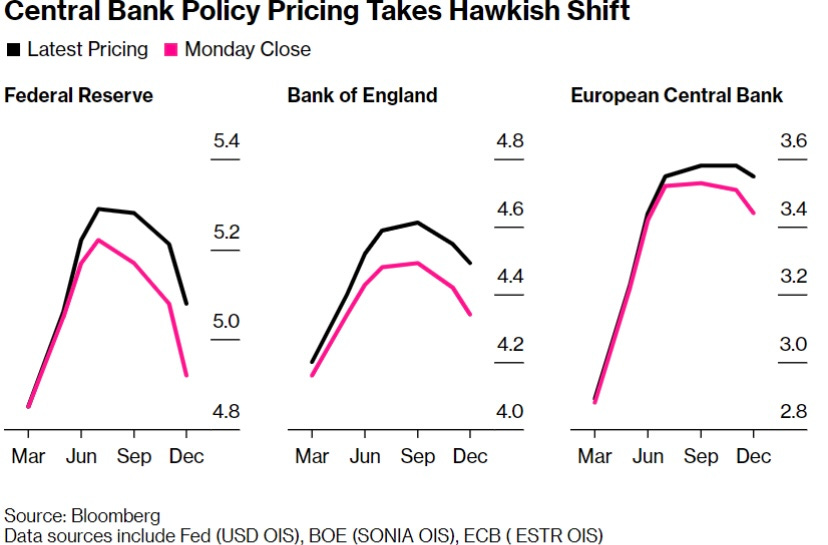

Three of the biggest are arguably some the most important Central Banks saw their Future Rates push back any projected cuts last week. These three Central Banks are the Federal Reserve (FED), Bank of England (BoE) and, the European Central Bank (ECB). As mentioned in the VIX section earlier in this newsletter we believe this change in Future rate pricing tightening is a sign market participants not just in the US are discounting the soft landing possibility. (Figure 13)

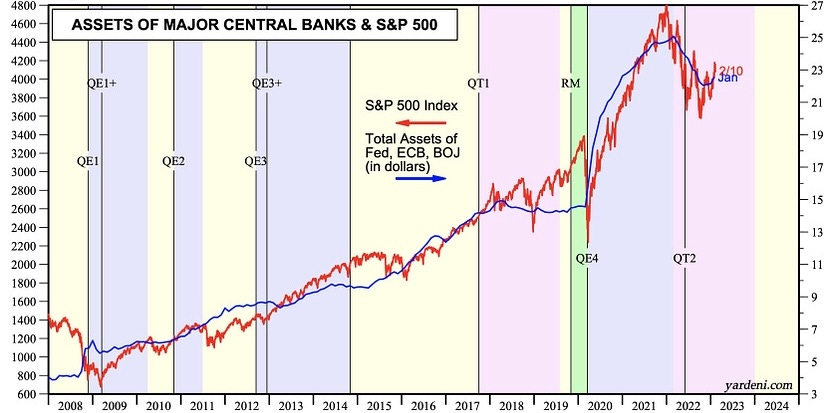

The FED does indeed have a long way to go, to bring inflation back to the goal of 2%. However even with everyone and their mother knowing that, the FED’s Quantitative Tightening (QT) program does not seem to be doing much. Well this is due to the Bank of Japan’s (BoJ) insane amount of Quantitative Easing (QE). In Fact the BoJ is buying show much of their own bonds to protect it’s bond yield ceiling. That this QE by the BoJ is canceling out all of the QT efforts by the FED, BoE and, ECB. This can be viewed visually by looking at Figure 13. It is our view (and many others) that the FED’s QT program is nowhere as strong as it needs to be. However, that is a story for another newsletter.

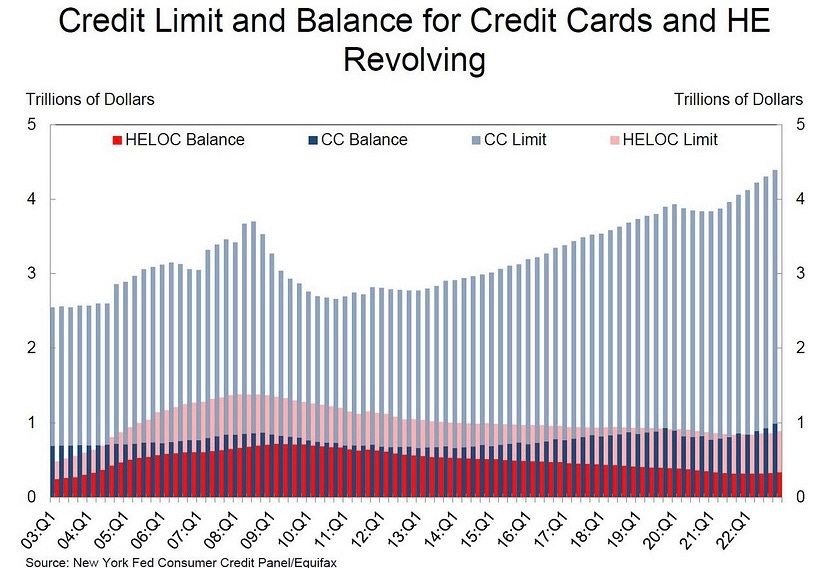

The Strong Consumer?

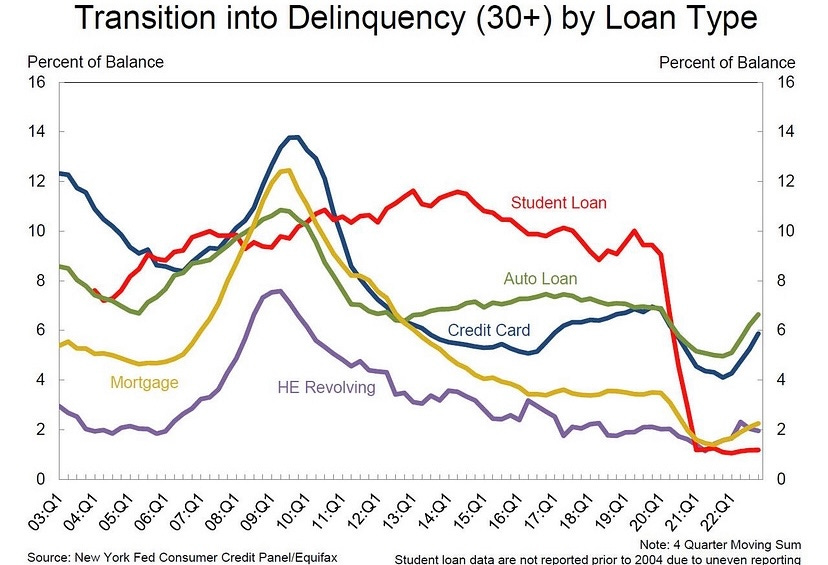

The American consumer has shown surprising strength (so far) during this hike in inflation. This strength is slowly starting to fade away. Most would agree that the government stimulus during 2020 helped keep the US consumer strong during the inflation we our now experiencing now. Also during this time (2020) borrowing money was very easy. In our opinion this lead to some Americans spending a large amount to their credit cards. We will let the reader decide if this increase in credit card spending is enough for alarm. (Figure 15) Along with this increase in spending is an increase in loans transitioning into delinquency. This can be seen clearly in Figure 16, with auto loans and credit cards leading the uptick in transitioning into delinquency. In closing more data is needed to truly determine if the US consumer is weakening.

DISCLAIMER: We are not Financial Advisors, and all information presented is for educational purposes ONLY. Financial markets can be extremely volatile, as such using good risk management is a must.