Market Malarkey 4/16-4/21

Weekly Market Updates & More

This week we are trying a slight adaptation to Market Malarkey. Our goal is to slim down some unnecessary content & only bring you the most important information. As always we are open to any & all feedback in the comments!

Rundown from last week (4/10-4/14):

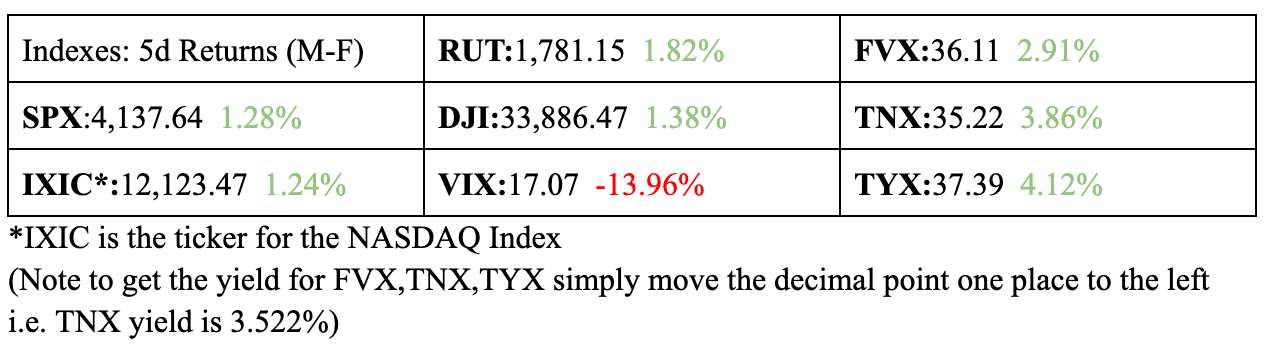

This past trading week was extremely choppy for US equity indexes until Thursday the 13th. With the S&P 500 (SPX) breaking out of a sideways channel on Thursday & rallying to a high of 4163.19 during Fridays open. (Figure 2) Even after a choppy weak for the equity markets all major indexes gained at least 1.25%. (Figure 1) With the RUT leading the way up 1.82% & the VIX continuing to fall. (Figure 1) Interestingly, all of the US Treasury yields (USTs) indexes also ended this past trading week up. (Figure 1) Also a quick aside, the VIX is $1.04 away from it’s 52W low.

Also of note some major US Banks beat their ER estimates, which seemed to help ease market participants fear about the banking “issue” spreading.

Preview for this week:

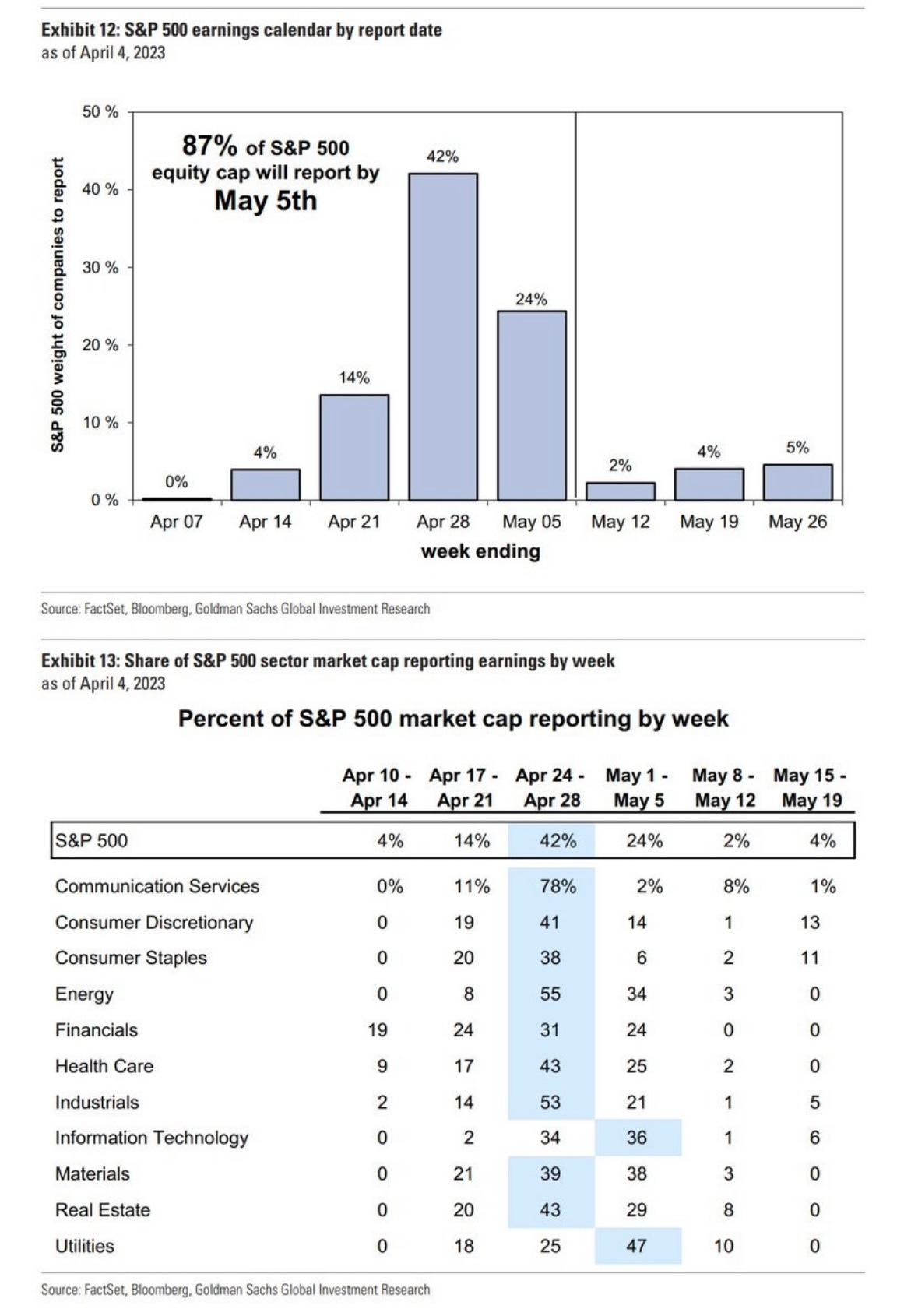

Speaking of earnings releases (ERs) the next few weeks are chock full of them with 87% of the S&P 500 will report ERs by May 5th. (Figure 3)

This upcoming trading week there are a slew of ERs from banks, other financial services, tech, and healthcare. (Figure 3)

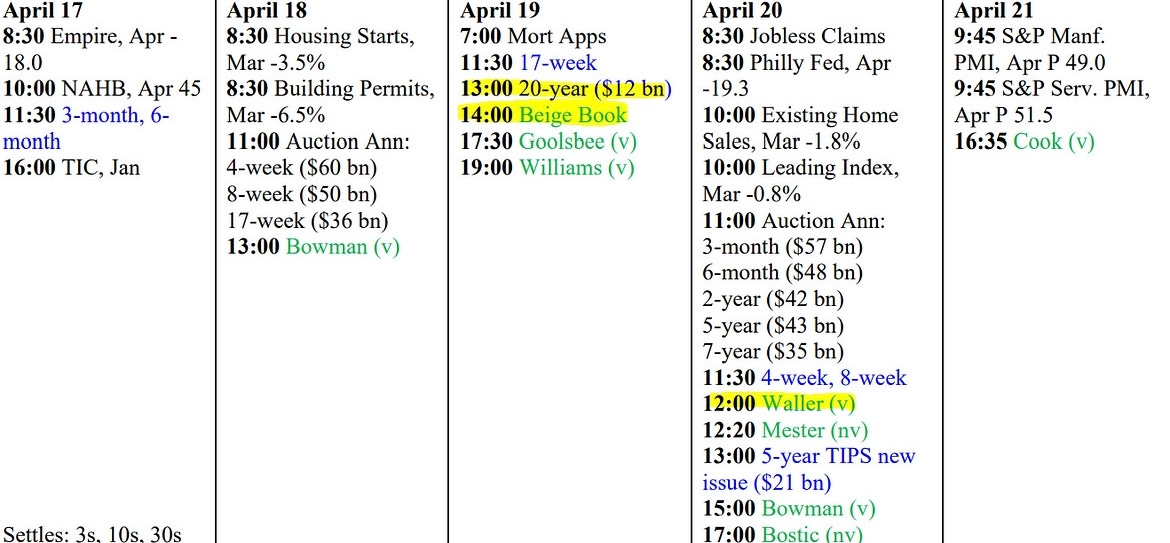

Economic data in the US is likely, in our view to take a back seat to FED speakers as this is the last week before the FED blackout period. As shown in Figure 5 by the

definitely subscribe to him, he writes a great newsletter. In the figure you will see greentext with either (v) or (nv), these are names of FED speakers both voting (v) and non voting (nv). (Figure 5) In the US, the financial market is currently divided on the likelihood of a potential interest rate hike by the Federal Reserve on May 3rd. Despite core inflation figures remaining high, the minutes of the Federal Open Market Committee (FOMC) meeting in March revealed that policymakers were cognizant of the risk that recent banking stresses could lead to tightened lending conditions and increase the likelihood of a recession. Nevertheless, officials remained optimistic and predicted that the fed funds target ceiling would end the year at a higher rate than its present level.Data releases in the upcoming week are unlikely to have a significant impact on market sentiment, as attention is likely to be focused on individual Federal Reserve officials. This is because they will have their last opportunity to express their views publicly prior to the pre-meeting blackout period in the days leading up to the May FOMC meeting. As we mentioned above. Given appropriate market conditions, it is highly probable that the Federal Reserve will choose to raise the policy rate at the May meeting. As such, it is crucial to closely monitor the statements and actions of the Federal Reserve members in the lead-up to the upcoming meeting. Even the non voting member Bostic has a history of effecting markets at least intra-day.

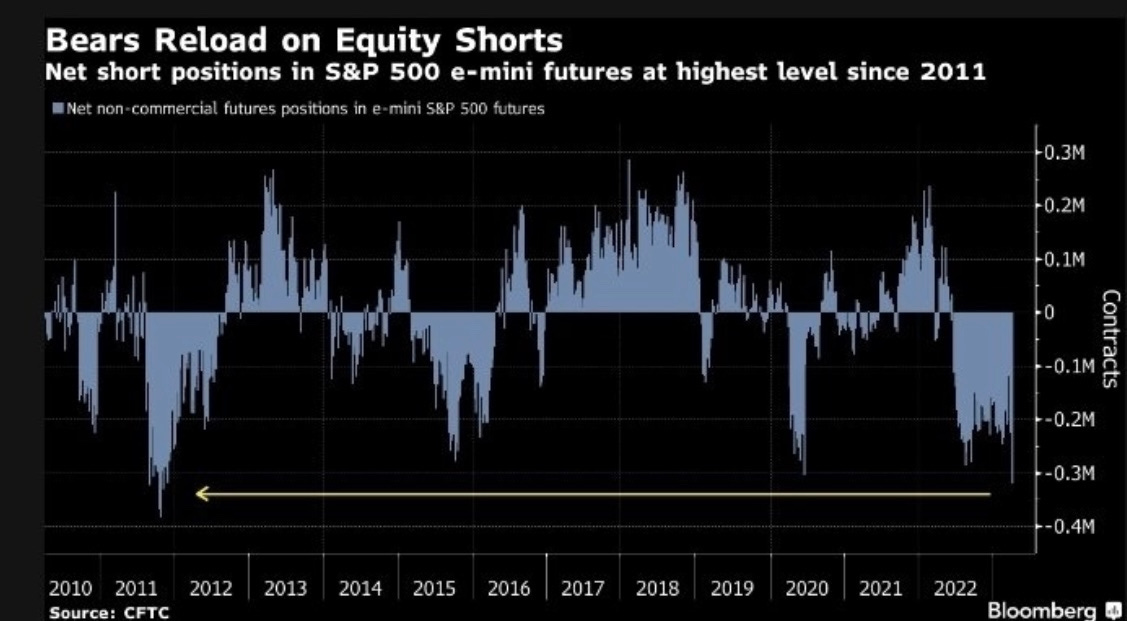

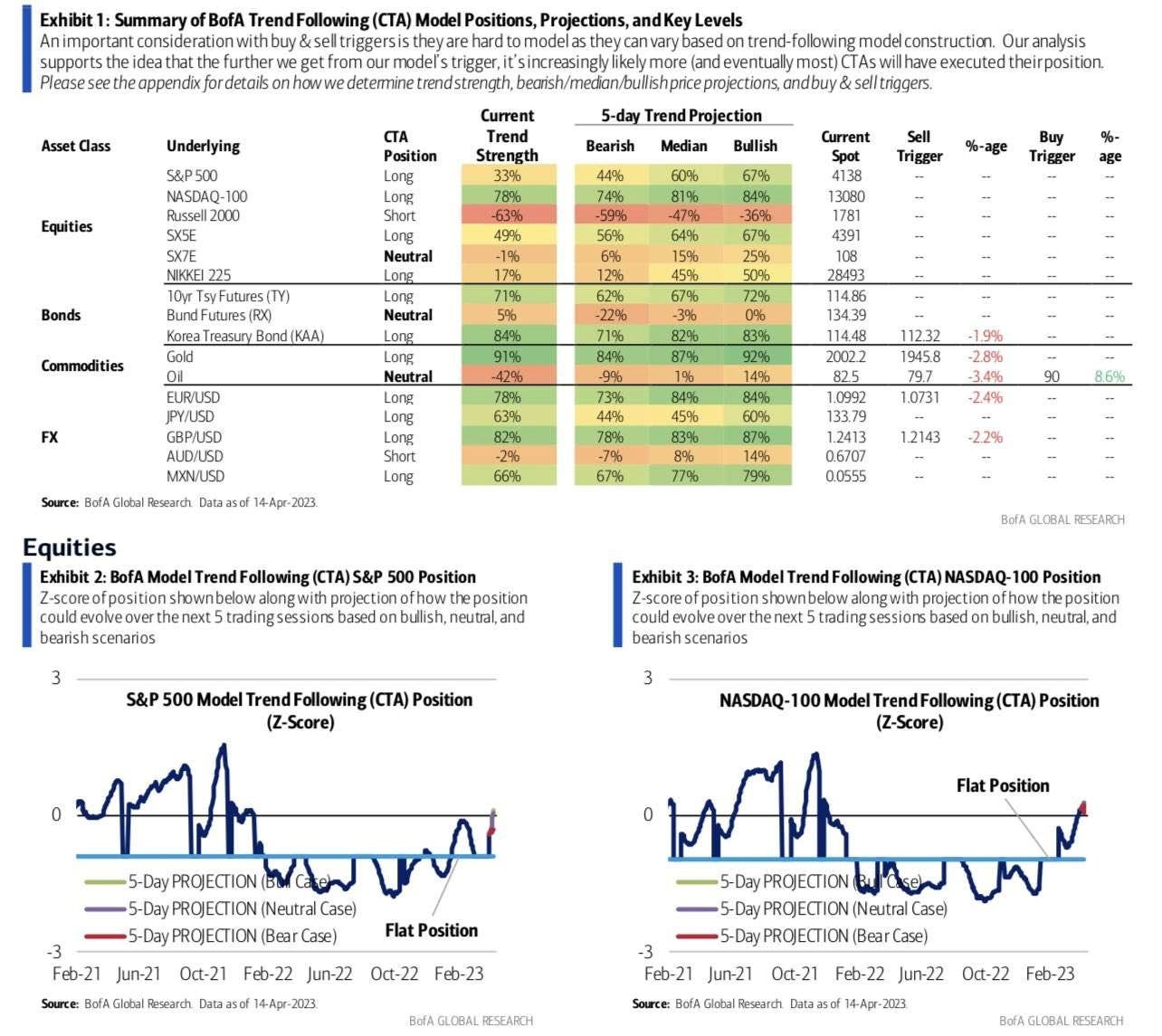

ES speculators are at their highest short level since 2011. (Figure 6) In our view this can add fuel to the equity market rally if the FED speakers this upcoming week are more dovish than market participants are expecting. Another factor leading us to be slightly bullish on the US equity market. Is the fact CTAs are long the the S&P 500 & NASDAQ. (Figure 7)

US Treasuries:

The 2Y UST yield appears to be recovering from its previous chop zone and is showing some strength. (Figure 8) That being said we expect the 2Y UST yield to retest 4.10% before getting rejected. It is likely then to re-enter the chop zone between 3.5%-3.8%. (Figure 8)

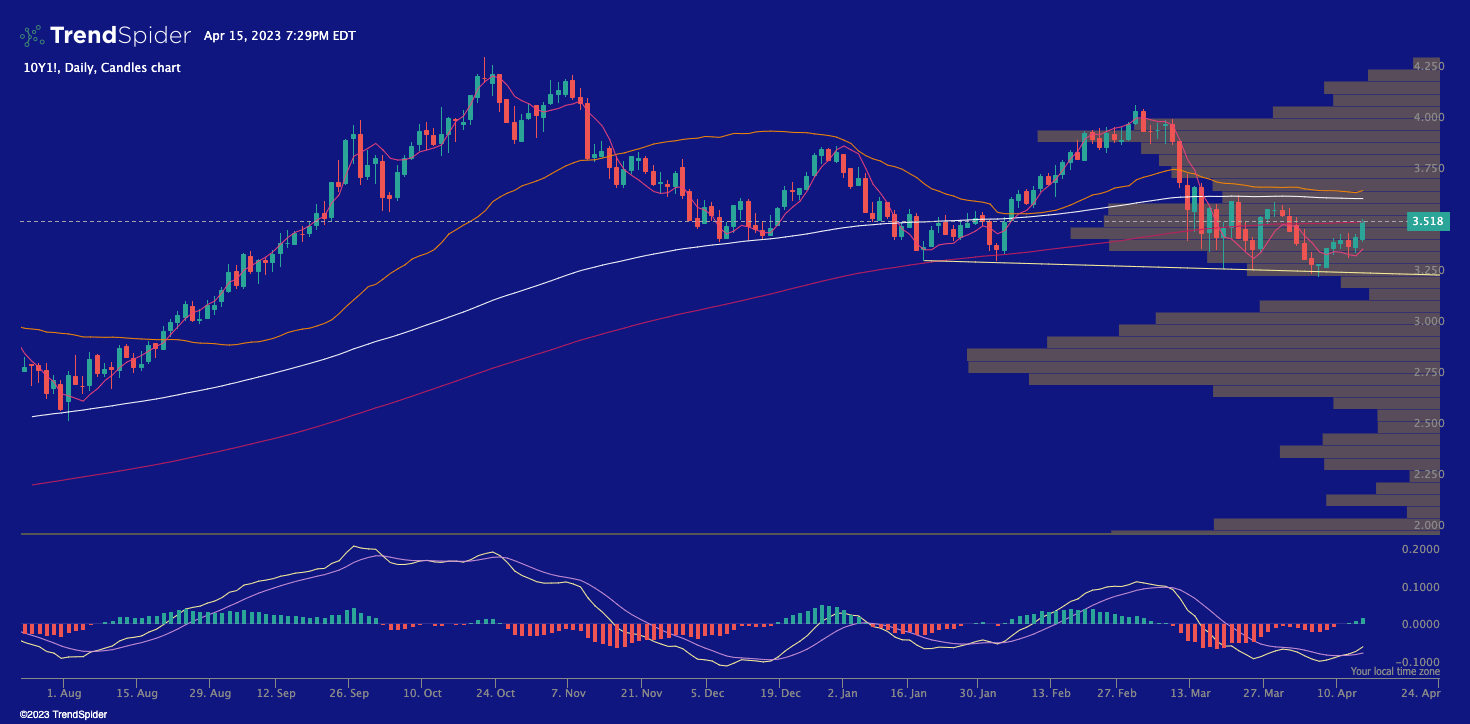

Much of the same applies to both the 2Y UST yield as well as the 10Y UST yield. We expect the 10Y to re-test the 200d WMA (white line), with a likely rejection there. (Figure 9)

Finally for the 30Y UST yield, perhaps the most interesting from a TA perspective. (Figure 10) In our view the bull case for the 30Y UST yield is a clean break and holding above the 200d WMA, with room to then run up near 3.85%. (Figure 10) The bear case is a hard rejection at the 200d WMA and re-testing the bottom trendline. (Figure 10)

Wrapping it up:

First we would like to say a big thank you to our new subscribers and all of our subscribers in general! In the coming days and weeks we have planned a small primer on biotech catalysts. Along with that we are working on the second article in the ‘Banking Blame Game’ series. As always thank you for reading and any feedback positive or negative is welcomed in the comments or on Twitter @cluelessfund.

DISCLAIMER: We are not Financial Advisors, and all information presented is for educational purposes ONLY. Financial markets can be extremely volatile, as such using good risk management is a must.