Market Malarkey 3/19-3/24

A wild week for the markets is coming.

Rundown from last week:

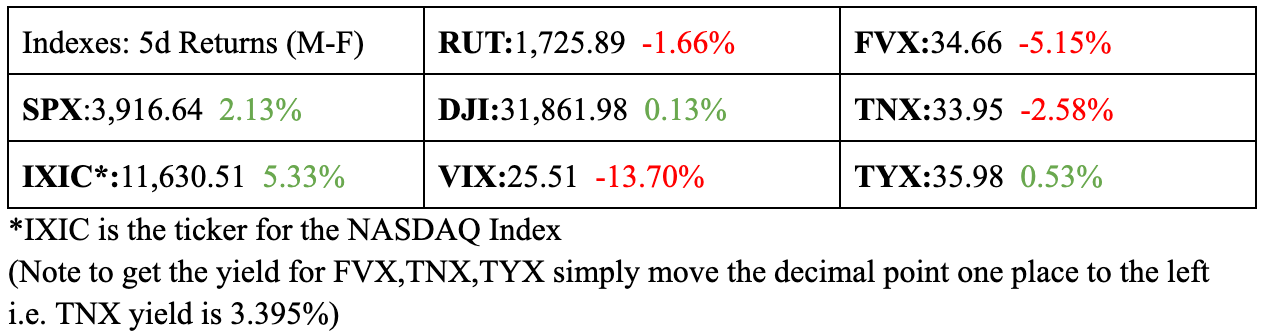

We plan on keeping this section as short as possible for a few reasons. The first of which is the fact the team was away from their desks until Wednesday. Secondly the amount of news to cover from this past week would take hours to fully explain. But onto the index review, US equity indexes continue to show strength given the currents taking place. The NASDAQ composite (IXIC) led the way for equities gaining more than 5% this past week. US treasury yields fell, excluding the 30Y. Finally the VIX also was in play this past week.

Preview for this week:

This is certainly going to be a very important one for the futures of the markets. The weekend brought much chaos, with UBS agreeing to buy CS for more than $2bn according to the Financial Times. This is a massive discount compared to the market cap of CS on Fridays close which was about $9bn, to us this is a very concerning sign that tells us CS books had to be pretty ugly. UBS also received a $100bn Swiss franc liquidity of credit from the SNB. We will expand on this and what we think it means in our Marco overview section.

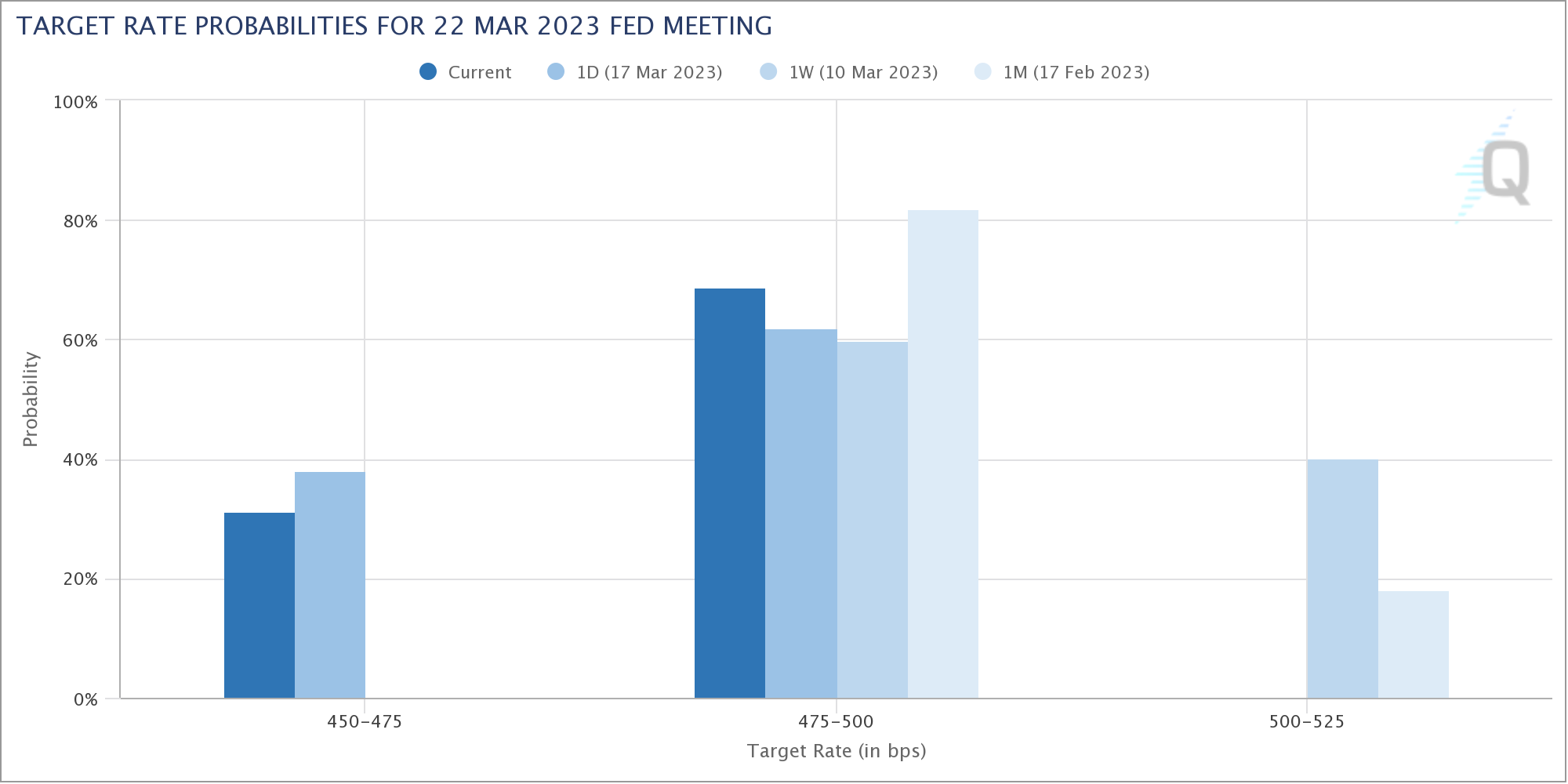

For the upcoming economic events all eyes are certainly on the upcoming FOMC meeting and rate release on Wednesday. (Figure 2) The markets are currently pricing in a 25 bps rate hike with a 68.6% at the time of writing (10:52 pm EST). The rest of the of the weeks economic calendar can be seen below in Figure 2.

Going back to the FED meeting probabilities for this coming Wednesday the changes in probabilities is striking. (Figure 3) The narrative currently is that the FED should slow their interest rate hikes and that a 50 BPS raise at the Wednesday meeting. While we agree with probability of a 25 BPS at Wednesday’s meeting is the most likely outcome for the FOMC meeting, we believe a 50 BPS raise would be the better solution. (We will expand on why we believe this in the Marco overview)

A pretty light week for earnings releases (ERs). Some interesting ERs this week include NKE & GME on Tuesday AH. (Figure 4) On Wednesday for ERs we have WOOF BMO and AH we have CHWY. (Figure 4)

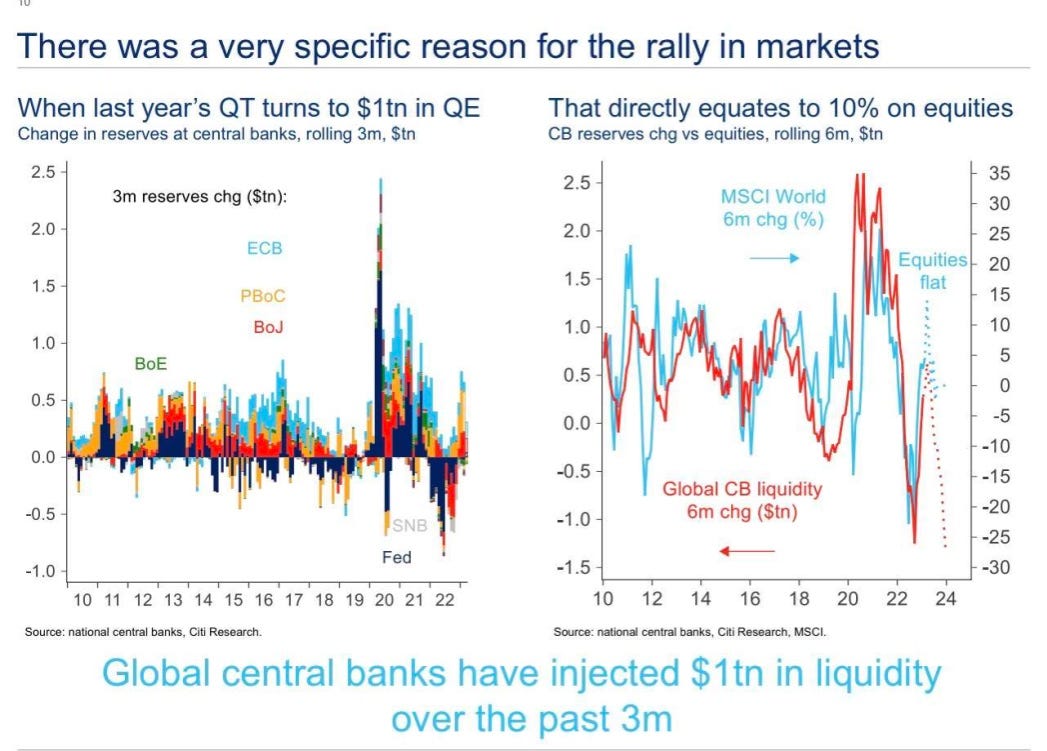

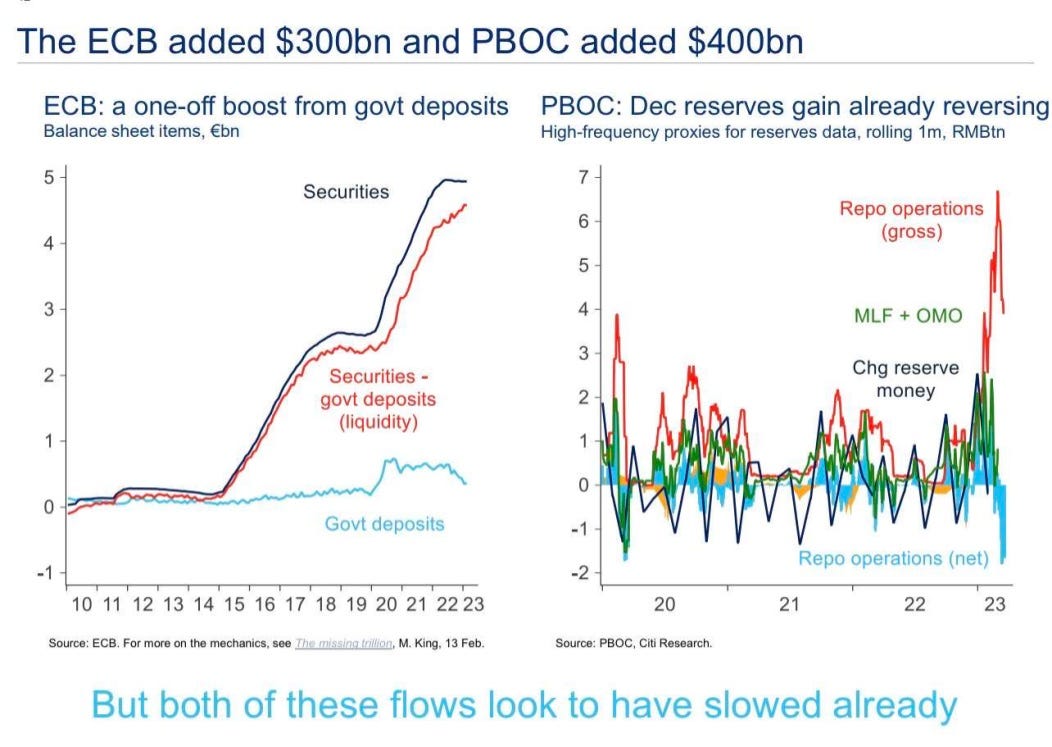

We would like to also highlight a solid hypothesis for this years earlier seemingly random rally and its strength despite high inflation in the US and globally. This can be seen in Figure 5, which shows the YTD currently at 2.43% and the rally which reached 9.7%. (Figure 5) We and many other believe that the reason for this CB QE. Here is some evidence for this idea that can be seen in Figure 6 & Figure 7. This liquidity is now we believe instead being offered to banks.

It is our view that this coming trading week is likely to be very volatile at least until after the FOMC decision. Bank stocks, especially regional banks are likely to be hit the hardest. We will be watching how the market reacts to the UBS buyout of CS, the dollar will also be on something we keep an eye on. Crude is nearing it’s 52w low based on the banking scares, we believe this is another important thing to watch this week. Finally we will be watching certain key credit spreads including BBB - AAA Corporate bond yield spread along with the CDS indexes.

US Treasuries & Fixed income:

For this week’s Market Malarkey we are going to do something it a little bit different first we will not be focusing as much on the TA aspect for US Treasuries. (USTs) This will still be a component of this section just not as in depth as before. The reasoning for this is we also want to highlight corporate bonds among other things. Let us know what you think of this change!

First up we have the 2Y UST yield futures. We added this because we realized we needed to take a look at a shorter dated UST. The 2Y UST has formed a double top as shown in Figure 8. We believe it is likely that the 2Y yield will re-test the 4.0% this trading week. (Figure 8) Both the 5Y UST (Figure 9) & 10Y (Figure 10) UST need a clean break of the 200d simple moving average (SMA) to rally during this trading week. If either the 5Y (Figure 9) or 10Y (Figure 10) can break their 200d SMA we see them rising to test their 200d weighted moving average (WMA). Finally we have the 30Y UST (Figure 11) we see the 30Y yield (Figure 11) bouncing between it’s 200d SMA & 200d WMA during this trading week.

Corporate bonds:

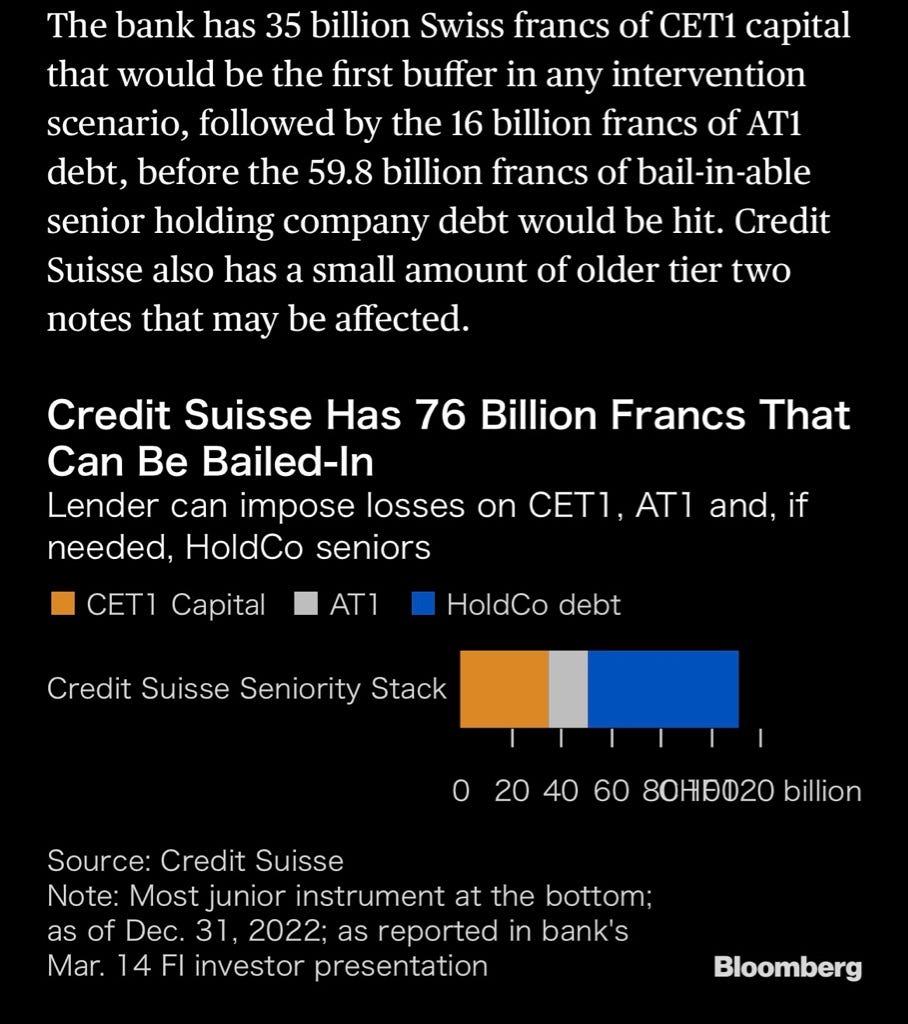

First we’d like to have a moment of silence for all of the CS additional tier 1 (AT1s) bond holders who got wiped out. In a somewhat rare move the SNB decided to protect shareholders before bond holders.

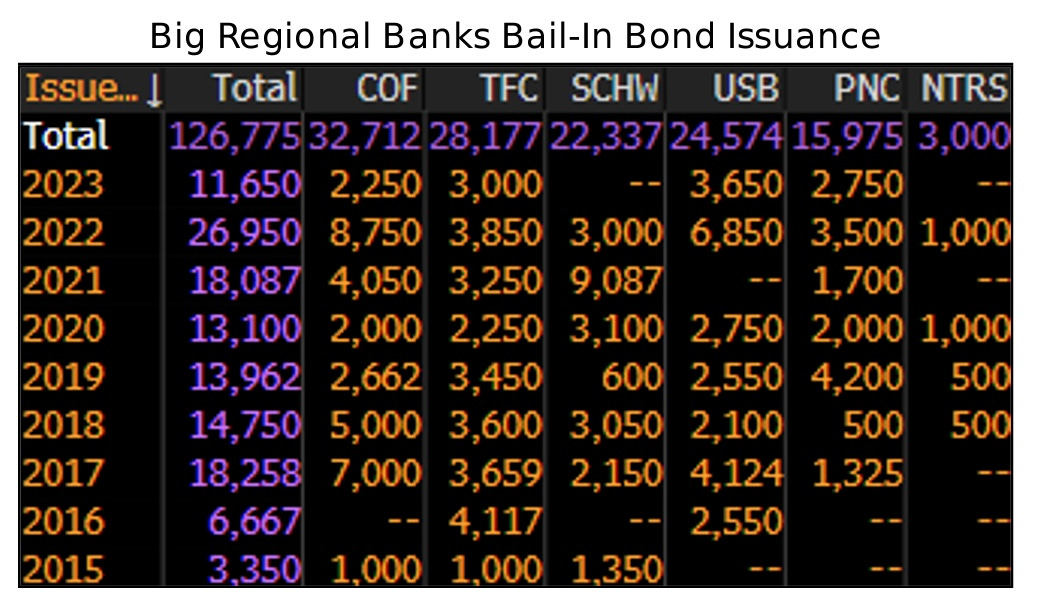

Next up for corporate bonds we would like to highlight that many regional banks are gearing up to issue more debt this year than any other since 2015. (Figure 13) With two of the banks already issuing more bail-in bonds this year than their yearly average from 2023-2015 would project for the entire year. (Figure 13) These are USB & PNC with an average yearly bail-in bonds being 2,730 & 1,775 respectively. That means both PNC and USB have issued around 900 more bail-in bonds then they normally would in a year. (Figure 13)

Possible trades & Follow ups:

We will not spend too much time going over are trade setup from our last Market Malarkey since we did that here.

Onto the trades we like this week. The first trade we would like to highlight is shorting US regional banks, we know not the most creative trade. We personally would go short on USB or CMA but any regional bank works. The second trade we would like to highlight is to go long on fixed income, we will hopefully finish a piece on solid fixed income assets.

Marco overview & our view:

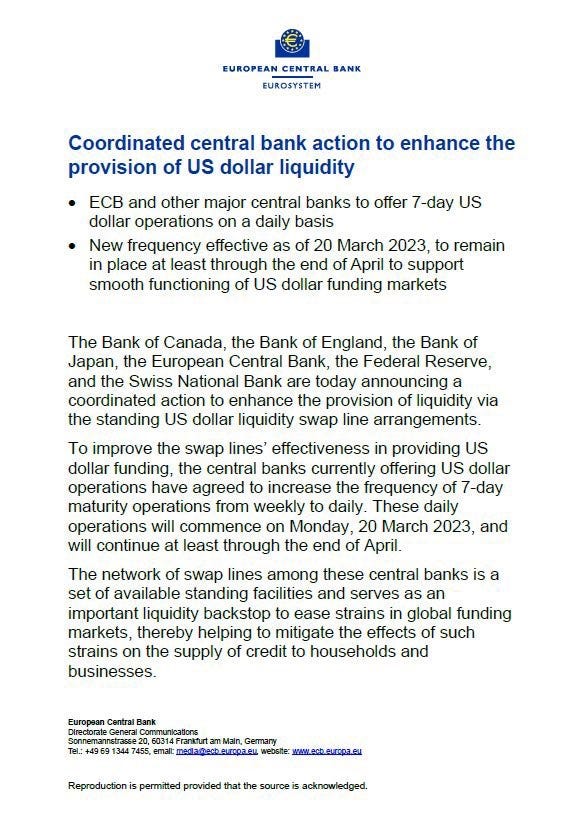

We believe that this banking situation is very far from over and has the possibility of kicking off something much, much larger. The announcement of daily swap lines between the major CBs also does not inspire a lot of hope for a soft landing. (Figure 14)

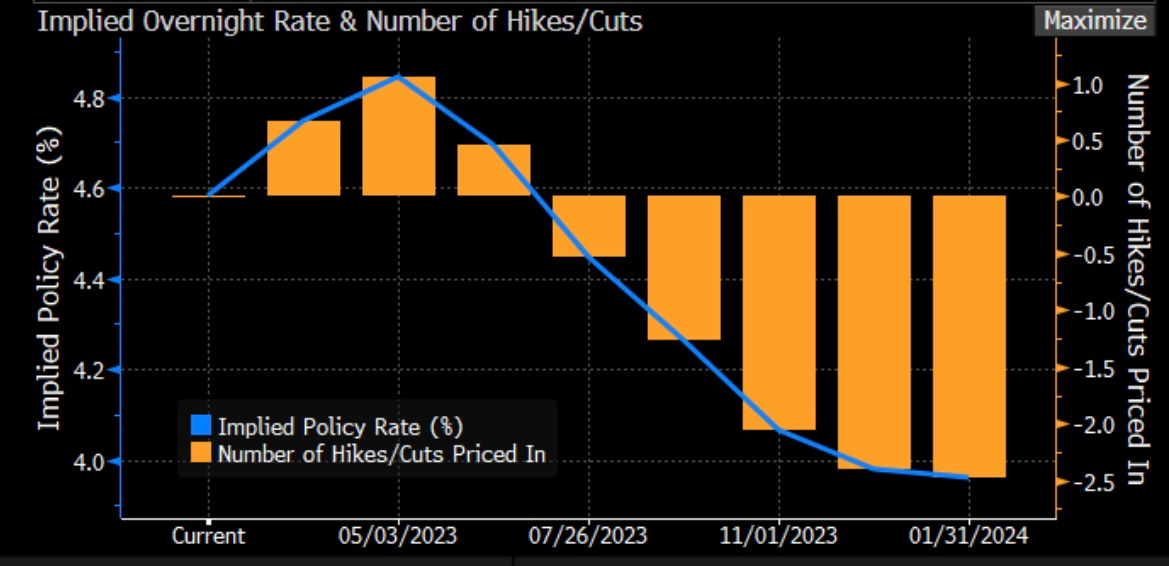

As mentioned earlier in the newsletter we believe that Powell should raise 50 BPS on Wednesday. This is probably unthinkable to most, however in our view it is better to get goal of 5% sooner rather than later. Bringing down inflation is more important than trying to save failing banks. We also strongly disagree with the market and believe the cuts it has priced in are much to kind. (Figure 15)

That is all for this week. Thank you for reading and please do let me know your thoughts!

DISCLAIMER: We are not Financial Advisors, and all information presented is for educational purposes ONLY. Financial markets can be extremely volatile, as such using good risk management is a must.