ERs & BoE Meeting

Hello everyone, I hope this week has been filled with good trades and good times. I’m still working on the Modern Monetary Theory (MMT) primer. It is taking longer than I expected but I think the end product will be worth the time. Also if you missed it I also started a chat for everyone, the first post in the chat is about safe haven assets. To join the chat, you’ll need to download or have the Substack app, available for both iOS and Android. Chats are sent via the app, not email, so turn on push notifications so you don’t miss conversation as it happens.

How to join the conversation

Download the app by clicking this link or the button below. Substack Chat is available on both iOS and Android.

Open the app and tap the Chat icon. It looks like two bubbles in the bottom bar, and you’ll see a row for my chat inside.

That’s it! Jump into my thread to say hi, and if you have any issues, check out Substack’s FAQ. With that let’s get into the article.

Earnings:

As you are likely aware of earnings season is in full swing. Banks along with many other notable companies already have reported their earnings. However, Thursday November 2nd (tomorrow at the time of writing) is filled with interesting earings. Both pre-market (PM) and after hours (AH). With everyone’s seemingly favorite stock AAPL 0.00%↑ reporting it’s ER AH. This of course will be a large catalyst for markets in my opinion. With that being said I am more interested in MRNA 0.00%↑ ER, along with LLY 0.00%↑ & NVO 0.00%↑.

Another two ERs I will be keen on reading the 10-K for PENN 0.00%↑ and DKNG 0.00%↑. Both also report Thursday November 2nd, I am thinking about possibly opening a long short (L/S) trade PENN 0.00%↑/DKNG 0.00%↑. If I decide to do this trade I will write an article with my reasoning.(Figure 2)

NVO 0.00%↑ released this bit of information a week or so ago. Novo Nordisk, has recently revised its sales and profit projections for 2023. The updated outlook at constant exchange rates (CER) shows an increased sales growth range, now ranging from 32% to 38%, up from the previous range of 27% to 33%. Additionally, the profit range has been adjusted to 40% to 46%, as opposed to the earlier projection of 31% to 37%. This revision is attributed to better-than-expected sales of Ozempic and Wegovy, which have positively influenced the company's guidance. This along with the hype behind Ozempic and Wegovy. It will be interesting to see what price NVO 0.00%↑ closes at tomorrow. Figure 3 looks back at history to determine possible outcomes, I disagree with the model. As you can see in Figure 4 on the 4H timeframe NVO 0.00%↑ is looking like it could re-test it’s all time high. (Assuming a positive earnings) A momentum model also fired off at the final close (including AH)

LLY 0.00%↑ has been one of the hottest stocks this year. With shares up 52% YTD and a potentially massive GLP-1 drug in the pipeline. It easy to understand the hype. Figure 5 includes my forecast forr LLY 0.00%↑ shares until December.

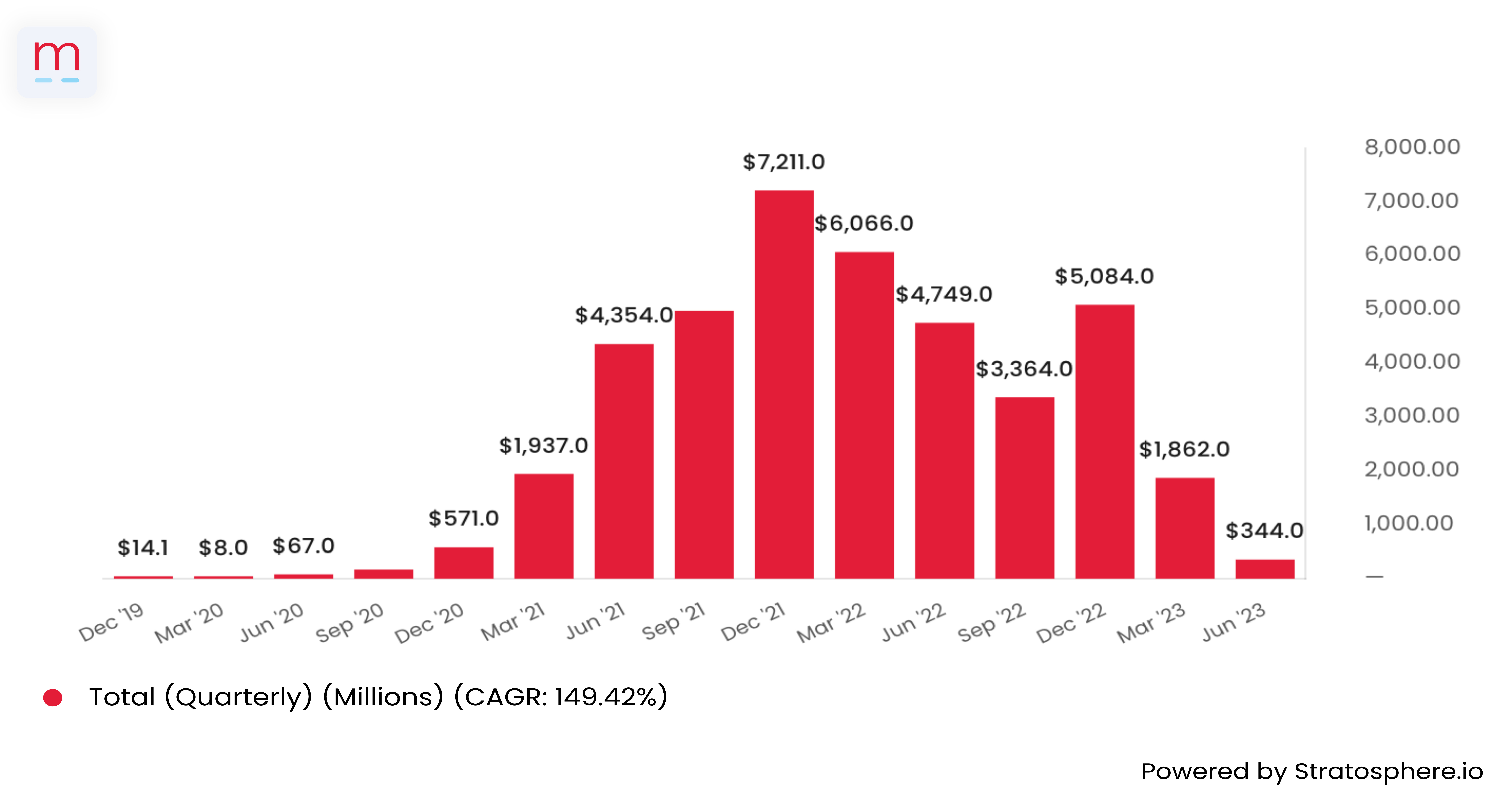

MRNA 0.00%↑ is in for a very bad Thursday in my view. With only COVID vaccines available for sale, MRNA 0.00%↑ has no moat to speak of. Figure 6 shows MRNA 0.00%↑ QoQ total revenue, you don’t need to be a sell-side analyst to understand this is bad.

As for MRNA 0.00%↑ I will just leave you with Figure 7.

BoE Meeting:

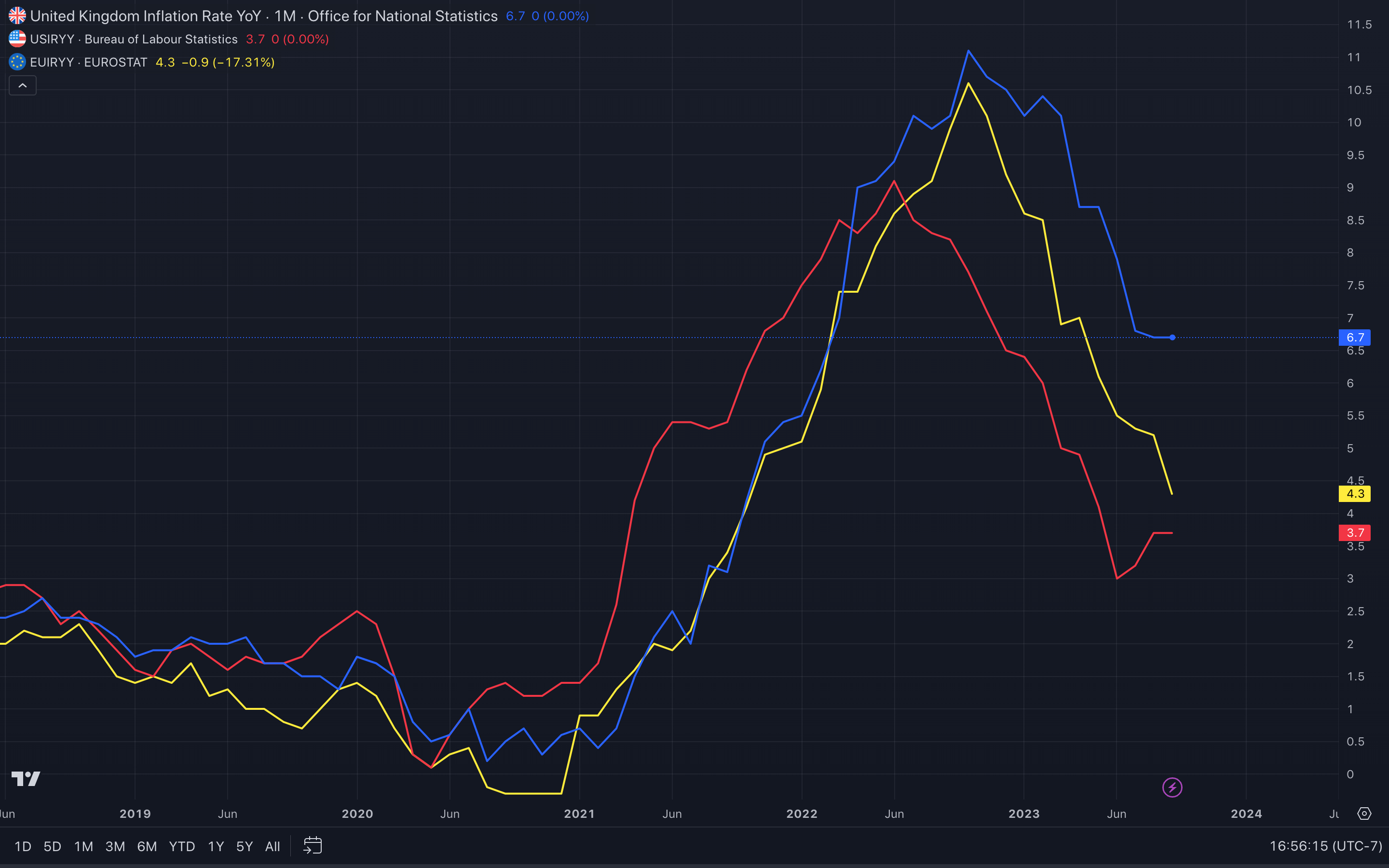

The United Kingdom haas been having a slightly harder time taming inflation when compared to the US and EU. (Figure 8) There is a widespread consensus among Economists that the Bank of England is highly likely to maintain the Bank Rate at its current level of 5.25% during the upcoming Thursday meeting. Market expectations align with this consensus, indicating that there is little to no anticipation of a policy rate adjustment during this meeting. However, there is a modest probability that a rate hike might be considered in several future meetings.

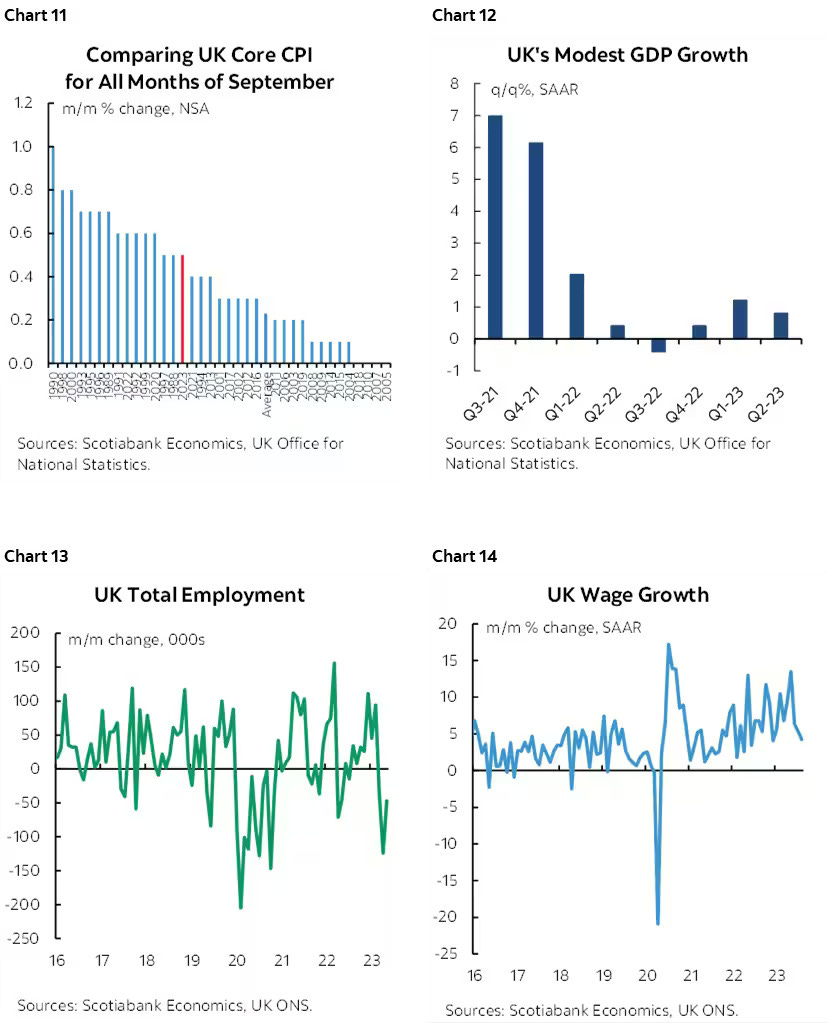

The core Consumer Price Index (CPI) pressures have cooled off from their previous intensity. GDP growth has experienced some setbacks. Job losses have become noticeable. Wage growth has recently moderated. Additionally, the gilts market has been impacted by the global bond market sell-off, in line with broader trends. Nevertheless, expect some Central Banker talk. These rants in theory serve the dual purpose of steering markets away from premature expectations of easing (which hasn’t worked so far). Along with expressing caution regarding the potential resurgence of inflationary pressures. The upcoming meeting will feature a fresh set of forecasts as well. While inflation has certainly cooled off a little bit when compared to the start of 2023. I think it is a mistake not raising rates by 25BPS at this meeting. With that said I under the reasons the ECB is likely to pause.

DISCLAIMER: We are not Financial Advisors, and all information presented is for educational purposes ONLY. Financial markets can be highly volatile, so good risk management is a must.

thank you, great coverage, cheers!