Distressed Debt

Distressed Debt

Looking at how distressed debt performed last month & some trade setups

Hello everyone, welcome back today we will be covering one of the sides of trading which interests me the most. As you can read from the title this is the distressed debt sector. What exactly is distressed debt?

Distressed debt refers to the securities of a government or company that has either defaulted, is under bankruptcy protection, or is in financial distress and moving toward the aforementioned situations in the near future.-CFI

These types of distressed debts come in many shapes including bonds which are the focus of this article. However, distressed debt can also come in the form of bank debt, trade claims and any other form of credit that meets the definition from the CFI. This article will explore some interesting developments across the corporate bond market, mostly the distressed kind.

The current lay off the land:

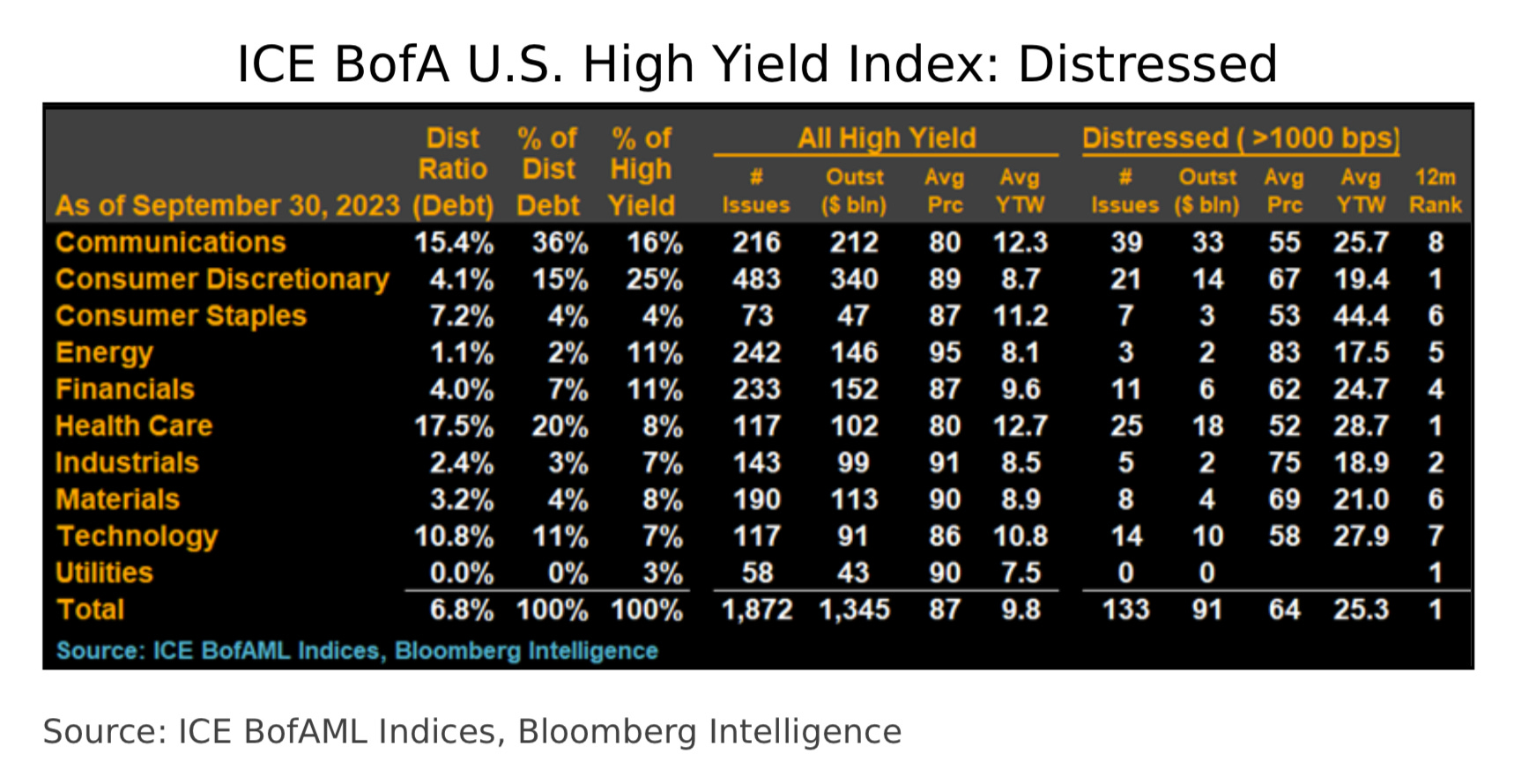

Interestingly distressed debt did not see an increase or decrease as a percentage in the ICE BofA US High-Yield Index between August and September. With the level of distressed debt in the Index staying level at 6.8%. The ICE BofA US High-Yield Index ratio of distressed bonds is under its previous low of 7.2% (which happened in August of 2022). Below in Figure one you can see a useful table which breaks down the Index by sector. We will comeback to this table so do not forget it.

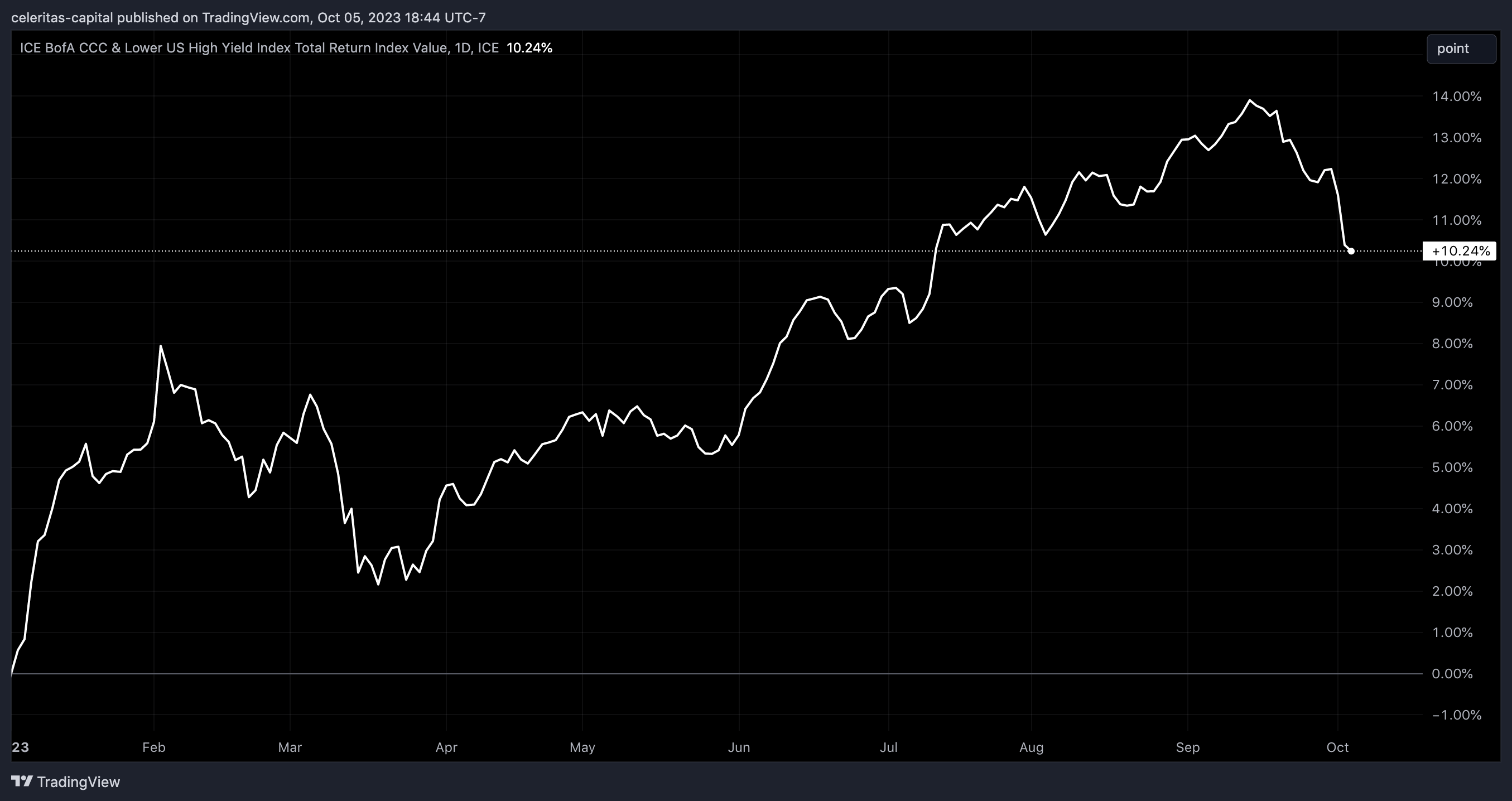

Distressed debt as measured by the ICE BofA CCC & Lower US High Yield Index has returned 10.24% YTD. (Figure 2) This performance is impressive, I believe distressed debt and High Yield bonds might not have topped this year.

To be clear I do not think this will turn into a junk bond rally but something more like a retest of the YTD high. My reasoning for this possible retest of the yearly high of around 17% is this. The idea was brought to my attention by

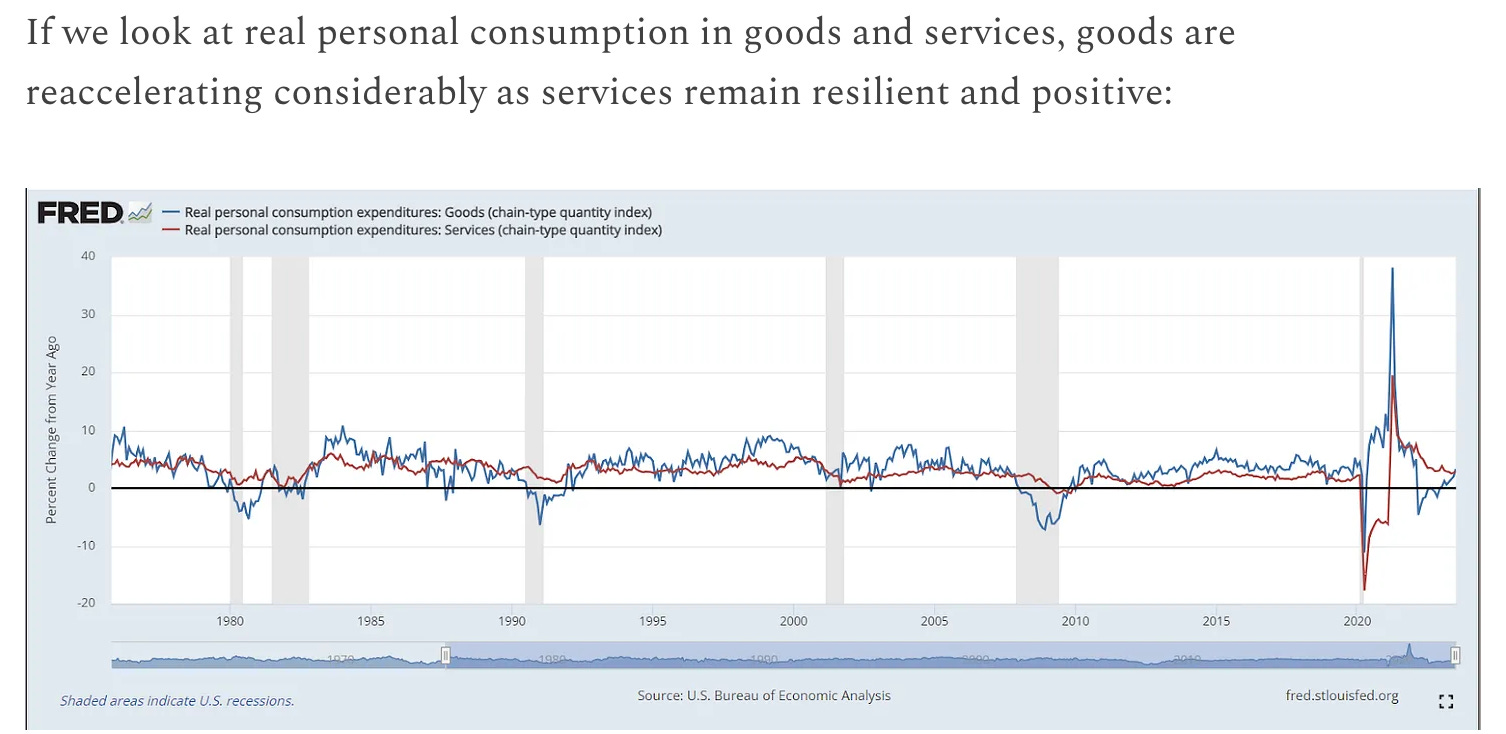

in his latest macro report which I recommend you read. In the repot lays out a very compelling case for the economy still has strong consumer element. That can be seen in the accelerating prenect of goods and the strength of the service industry.1 How does this help distressed bonds you might be asking? Well no signs of an official rescission in the near term, I believe fund managers will have no problem chasing risky trades so they end the year with a performance better than the market.

With that explained, I would be remiss if I did not also bring up the fact that a handful of bonds in the index will probably carry the index. So now lets review last month’s best & worst performers, then we will explore some of the possible setups for the coming months. Cano Health's unsecured notes, totaling $300 million and carrying an interest rate of 6.25%, with a maturity date set for October 2028, demonstrated notable performance within the ICE BofA U.S. Distressed Index during the month of September. (Figure 4) These bonds experienced a significant increase of 10 points, reaching a valuation of 44 cents on the dollar by the end of the month. This uptrend was influenced by Cano Health's announcement on September 26th, where they disclosed the sale of all their senior-focused primary care centers in Texas and Nevada for a sum of $67 million. As part of their financial strategy, the company also intended to reduce its revolving debt by $80 million.

In a similar vein, Rakuten Group's issuance of $1 billion in perpetual notes, featuring a 6.25% interest rate and callable in 2031, stood out as a top-performing bonds in the Index this month of September. (Figure 4) The Japan-based e-commerce retailer's notes experienced a notable increase of 10 points, rising to a value of 61 during the month. This positive trajectory marked a continuation of the notes' climb, which began in July when they were valued as low as 41 cents on the dollar.

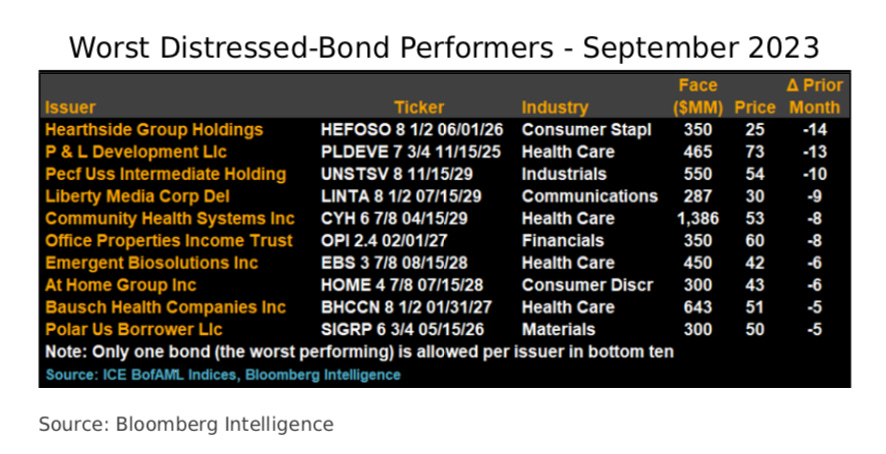

Now onto to the worst performers for the month of September. Hearthside Group's $350 million in 8.5% notes scheduled for maturity in June 2026 experienced a considerable decline of 14 points during the month of September, resulting in a valuation of 25 cents on the dollar. (Figure 5) This performance marked it as the poorest-performing asset in the ICE US Distressed Index for the month. The bonds of this private food manufacturer, which is under the ownership of Charlesbank and Partners Group, faced additional downward pressure towards the end of September. This decline was attributed to indications from the Biden administration suggesting potential actions against large employers of contractors, such as Hearthside, accused of violating child labor laws.

Similarly, P&L Development's $465 million worth of 7.75% notes, set to mature in November 2025, experienced a significant decrease of 11 points in their value during the month of September. (Figure 5) This performance ranked it as the weakest performer among the notes within the ICE US Distressed Index for the same period. These secured notes constitute a substantial portion of the capital structure of the private label health-care product manufacturer. In June, S&P had assigned a CCC+ rating to these secured notes with a negative outlook, citing significant concerns related to liquidity.

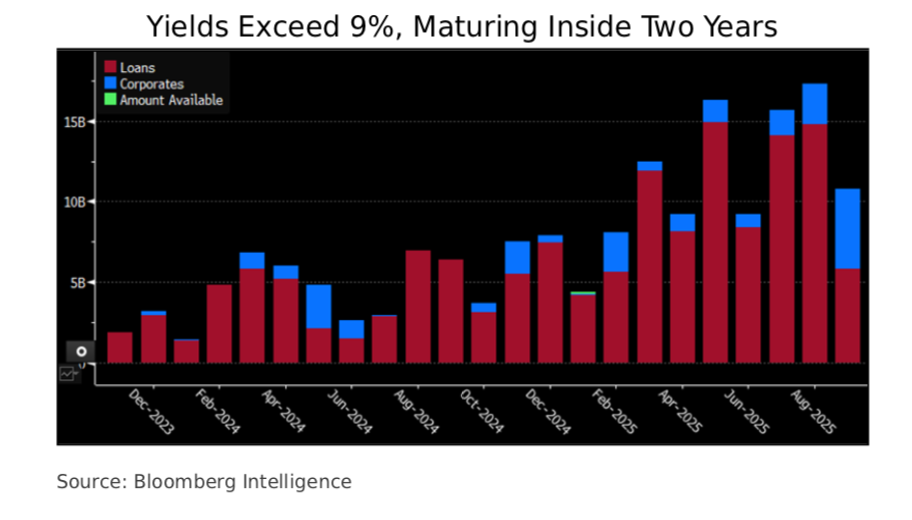

Now let’s take a quick at when some of this distressed debt matures. Of the North American bonds that yield more than 9% there is $5 billion maturing this year another $67 billion maturing in 2024 and a sizeable amount in 2025 of $120 billion maturing. The overwhelming amount of this distressed debt is in the form of loans, which can be seen in Figure 6.

Distressed Setups

Now let us explore some possible setups in the land of distressed debt. Before we do that however I believe it is always important to disclose if I am taking a position in any products I bring up. I will not be taking any of these trades as I unfortunately do not have the capital to fund such risky trades. I wanted that to be disclosed, also these trades are extremely risky in nature (if that hasn’t been clear throughout the article) so do not consider these trades if you are not prepared to loss all the capital you put into a trade.

With that all being said I would like to track my trade setup ideas. I’m thinking about creating a paper bond portfolio and sharing the results here. Please vote in the poll below and let me know if that is of any interest to you!

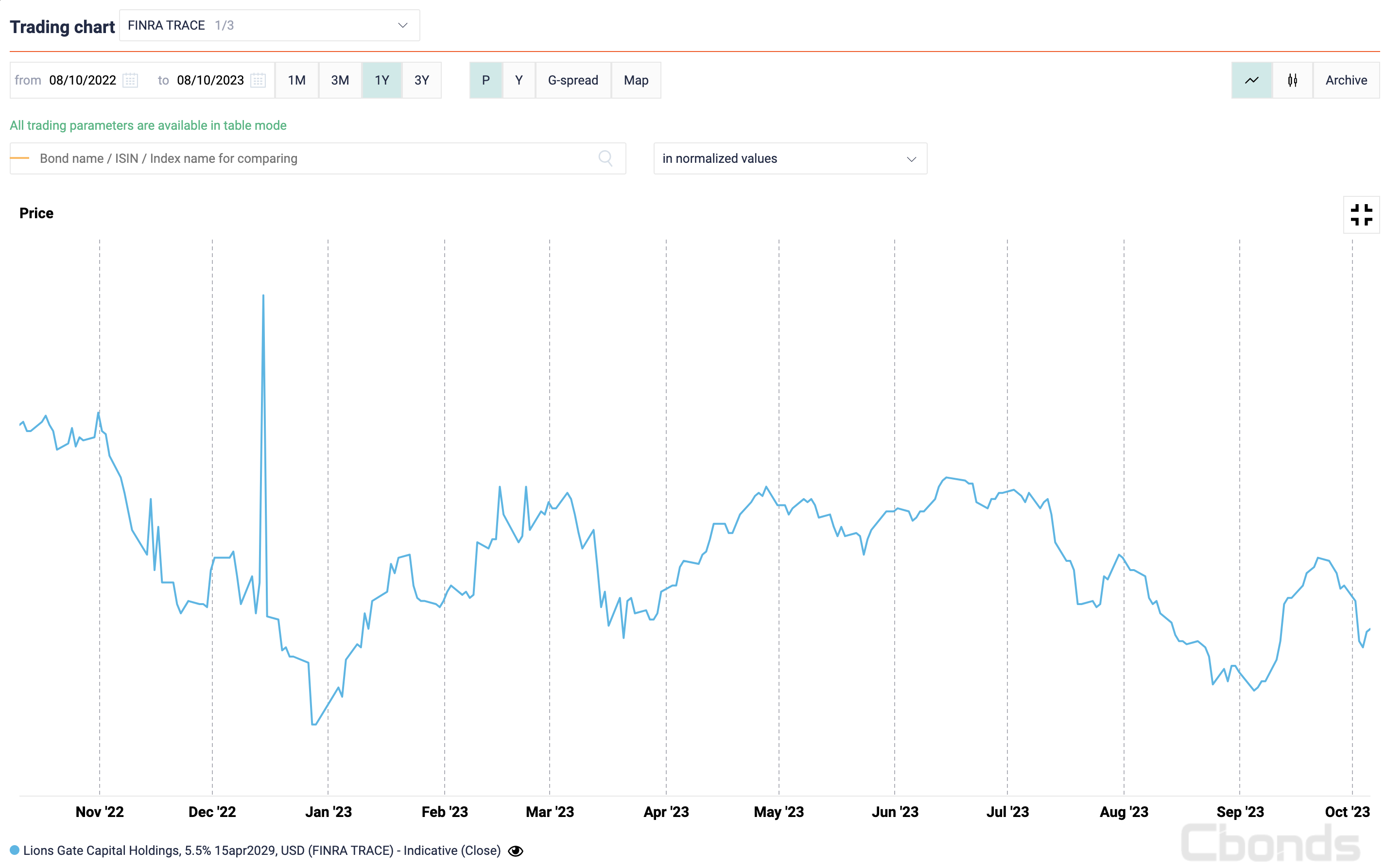

Lions Gate, 5.5% 4/15/29 (BUY)

While this bond rallied hard in September it started to loss a lot of its gain towards the end of the month. However with the writers strike ended and the actors strike likely to end soon I think this bond could rise back to it’s highs during September. (Figure 7)

Bristol Myers Squibb, 2.9% 7/26/24 (SELL)

On June 3rd 2022 Bristol Myers Squibb ($BMY) purchased Turning Point Therapeutics for $4.1 billion dollars. (Source) Today October 8th 2023 BMY 0.00%↑ has announce it’s agreed to buy Mirati Therapeutics for $4.8 billion. (Source) Figure 8 shows the price action for the BMY 0.00%↑ bond maturing 4/15/24 after June 3rd 2022 after their purchase of Turning Point Therapeutics. In the following weeks the bond fell in price approximately 1.5%. (Figure 8) I think that due to the extreme similarity in Turning Point Therapeutics and Mirati Therapeutics it’s likely the Bristol Myers Squibb, 2.9% 7/26/24 again drops in price temporarily.

Well that is all I have for today. I hope you learned something from this article or at least enjoyed reading it! A big thank you to all my new subscribers, if you have any suggestions please let me know in the comments or via email.

Inspired by work by Capital Flows so all credit to him. His macro report is brilliant

DISCLAIMER: We are not Financial Advisors, and all information presented is for educational purposes ONLY. Financial markets can be highly volatile, so good risk management is a must.

I'm not too familiar with distressed debt. Great article. I'd definitely follow a paper portfolio if you end up creating one. Great way to learn more.

Great piece and very well-written!!