Corporate Bond Primer (Part 1)

An introduction primer for the market of corporate bonds

Hello everyone, I am very excited to finally release my first Primer. For my first one I thought I would cover the often overlooked market of corporate bonds. I do hope you enjoy reading this primer as I spent a large amount of time both researching and writing this primer. As this topic is rather information filled I believe it is best to split this primer into three parts. I have tried my very best to make this primer understandable for someone who has zero previous knowledge about corporate bonds. However, as we progress into parts two & three the more detail we will explore. As always comments are more than welcome.

Part One- The Groundwork

Part Two- Risks related to corporate bonds

Part Three- Analyzing and trading corporate bonds

The Basics: Terminology and Definitions:

To understand corporate bonds (corp. bonds), it's essential to familiarize yourself with key terminology. Below is a list of some essential definitions for understanding the rest of this primer.

Issuer: The company or corporation that issues the bond.

Bondholder: The investor who purchases the bond and lends money to the issuer.

Face Value: The principal amount of the bond that will be repaid at maturity.

Coupon Rate: The fixed interest rate paid by the issuer to the bondholder.

Maturity Date: The date on which the issuer must repay the face value of the bond.

Yield: The rate of return on the bond based on its coupon rate and market price.

Secondary Market: The market where already-issued bonds are bought and sold.

Callable Bond: A bond that can be paid off by the issuer prior to its maturity date at a specified call price.

Yield to Maturity: The annual rate of return on a debt instrument purchased at a market price and held to maturity taking into consideration the coupon and pull to par of the bond.

Yield to Call: The yearly return of a bond bought at market and held to call, including coupon payments and price swings.

Yield to Worst: The least an investor can get back on a bond (short of issuer non-payment). Holding until the end or issuer buying it back early. Riskier bonds often let the issuer call them back and show their lowest possible return based on that. Less risky bonds typically show their return if the investor holds them till maturity, typically.

Duration: A bond’s sensitivity to changes in interest rates taking into consideration a bond’s maturity, yield, coupon, and call features. Bonds with longer maturities and lower coupons typically have longer durations/ greater interest rate sensitivity.

The Basics: Expanded:

This primer provides an overview of corporate bonds, including their basic terminology, reasons for issuance, the different types, associated risks, calls, credit ratings, and a synthesis of the key concepts. Corporate bonds are debt securities issued by companies to raise capital. They serve as a means for companies to borrow money from investors and pay them back with interest over a specified time horizon, on specific dates called the coupon payments. In the context of corporate bonds the word coupon payment refers to the annual interest paid on a bond. Investors are also repaid the original value of the bond known as the par value of the bond when it matures. Corporate bonds are mostly issued in denominations of $1,000 unless stated otherwise. The specific terms for payments, maturity and more can be found in the bonds prospectus. If the company fails to pay interest or principle the bondholders can enforce the contract via court proceedings. Bondholders as creditors have a prior legal claim over shareholders (and preferred shareholders) An example of a typical companies capital structure looks similar to Figure 1 below. I will expand on and explain in more detail each layer of the pyramid in Figure 1 in the next section of the premier.

Why Companies Issue Debt & What Types Exist There:

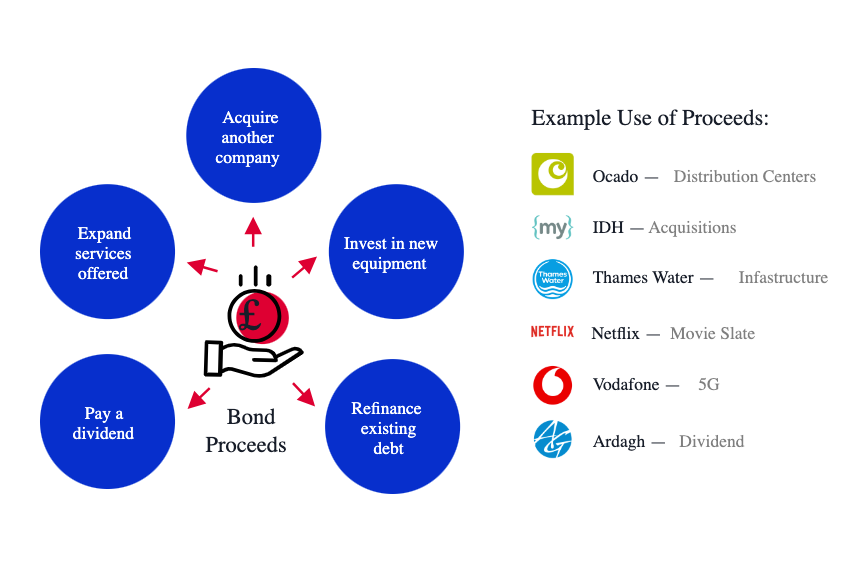

Companies issue debt through corporate bonds for various reasons, such as financing expansion, funding acquisitions, or refinancing existing debt. (Figure 2)

Types of bonds:

Senior Secured Bonds: In the world of corporate bonds “secured” debt/bonds are backed with some type of collateral by the issuer.The term senior in this context refers to bond takes primacy over any other company’s sources of capital. (Excluding secured corp. bonds) The most senior holders will always be the first to receive a payment if the company whose bond is being held defaults. (Figure 1 for a visual reference.)

Senior Unsecured Bonds: Senior unsecured bonds resemble their secured counterparts in all but one crucial aspect: they lack the safety net of collateral. Despite this, senior bondholders hold preferential claim in the event of a default.

Junior/Subordinated Bonds: Following the payout of senior securities, the next in line to receive compensation from residual assets are those holding junior/subordinate, unsecured debt. Without the assurance of collateral, these bonds depend heavily on the issuer's financial standing and credit rating. Their junior or subordinated position in the repayment hierarchy means they settle only after senior bonds have been fully addressed in a default.

Convertible Bonds: Are a type of bonds issued by companies that have the built in ability to be exchanged for common shares in the issussing company. Since these bonds are a type of hybrid security the price is influenced by the issuing company's stock and offering investor flexibility. With the added trade off of trading at lower yields than similar-sized standard bonds. This is due to the optionality of the convertible bonds.

Now that we’ve covered the main types of bonds it is time to take a look at the two broad grades of bonds. Investment grade (IG) and High yield (HY), sometimes called junk bonds as well. However, I will refer to them as High yield bonds as I do not like the image the word junk invokes for most.

Investment Grade: IG bonds include corporate bonds with a credit rating of BBB- or higher. These IG bonds are usually issued by companies with a lower risk of defaulting. Whether it be because they have a better balance sheet or they are an established name with a history with the credit rating agencies. Some data points for IG bond market includes that there is currently around $8 trillion IG corp. debt outstanding. Financials make up the largest sector of IG bonds. Most IG debt is issued with a fixed rate.

High Yield:

HY bonds are rated BB+ or lower and as one might guess bonds in the issuers of HY bonds are often at a high risk of defaulting. This can be due to macroeconomic headwinds a company is facing, along with high levels of leverage etc. Interestingly 28% of HY bonds are issued by private companies. Some data points on HY bonds include that currently there is $1.5 trillion in HY bonds outstanding. Consumer cyclicals companies are the largest issuers of HY bonds, a majority of HY bonds are also callable (more on callable bonds in the next section.) Most HY bonds also have a fixed rate like IG bonds.

Credit ratings & Calls:

Calls

So what exactly are calls in the world of corp. bonds? Calls are a part of the contractual agreement between bond issuers and holders. The call option allows the issuer to buy back the bonds before they mature for the par value plus 50% of the coupon. (Specifics depend on each individual bond issuance.) For example imagine company XYZ issued a 20Y maturity, non-callable until year 10. At year 10, company XYZ will have the option to call their bonds for par value plus 50% of the coupon. Why would a company want to do this? Well imagine the coupon payment for XYZ’s 20Y bond is 4.5%, if FED Funds are cut below that threshold to let’s say 2%. It makes a lot more sense for XYZ for call back their bonds and issue bonds with a lower coupon which means less interest XYZ has to pay to it’s bond holders.

Demystifying the Gatekeepers: A look at Credit Rating Agencies

Even for finance professionals, navigating the labyrinthine world of corporate bonds is a never ending pursuit. But even the most seasoned veterans rely on crucial intel to assess an issuer's creditworthiness. Enter the enigmatic entities known as credit rating agencies (CRAs), the gatekeepers who hold the keys to unlocking (or slamming shut) the doors to lucrative investment opportunities.

A Historical Exposé:

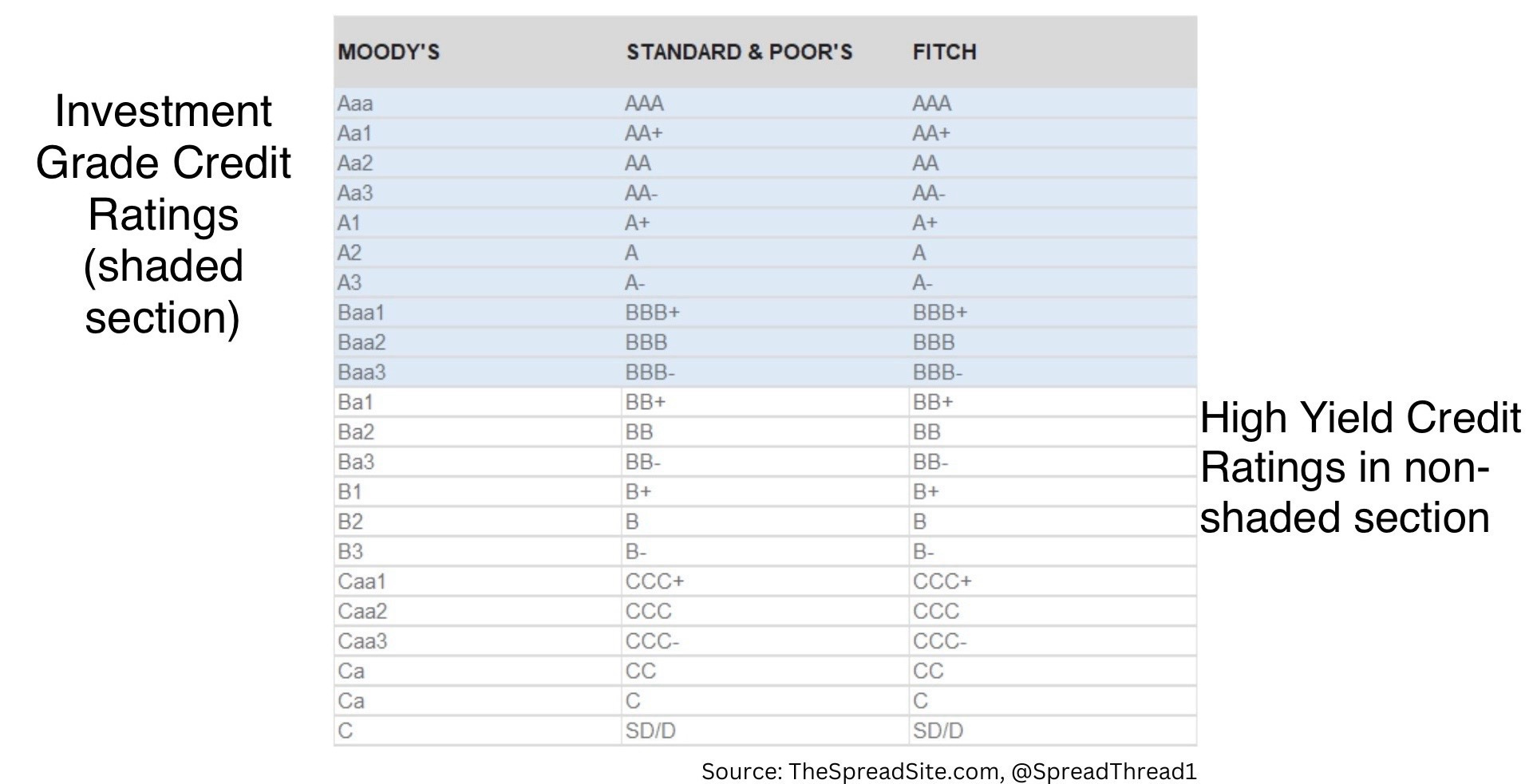

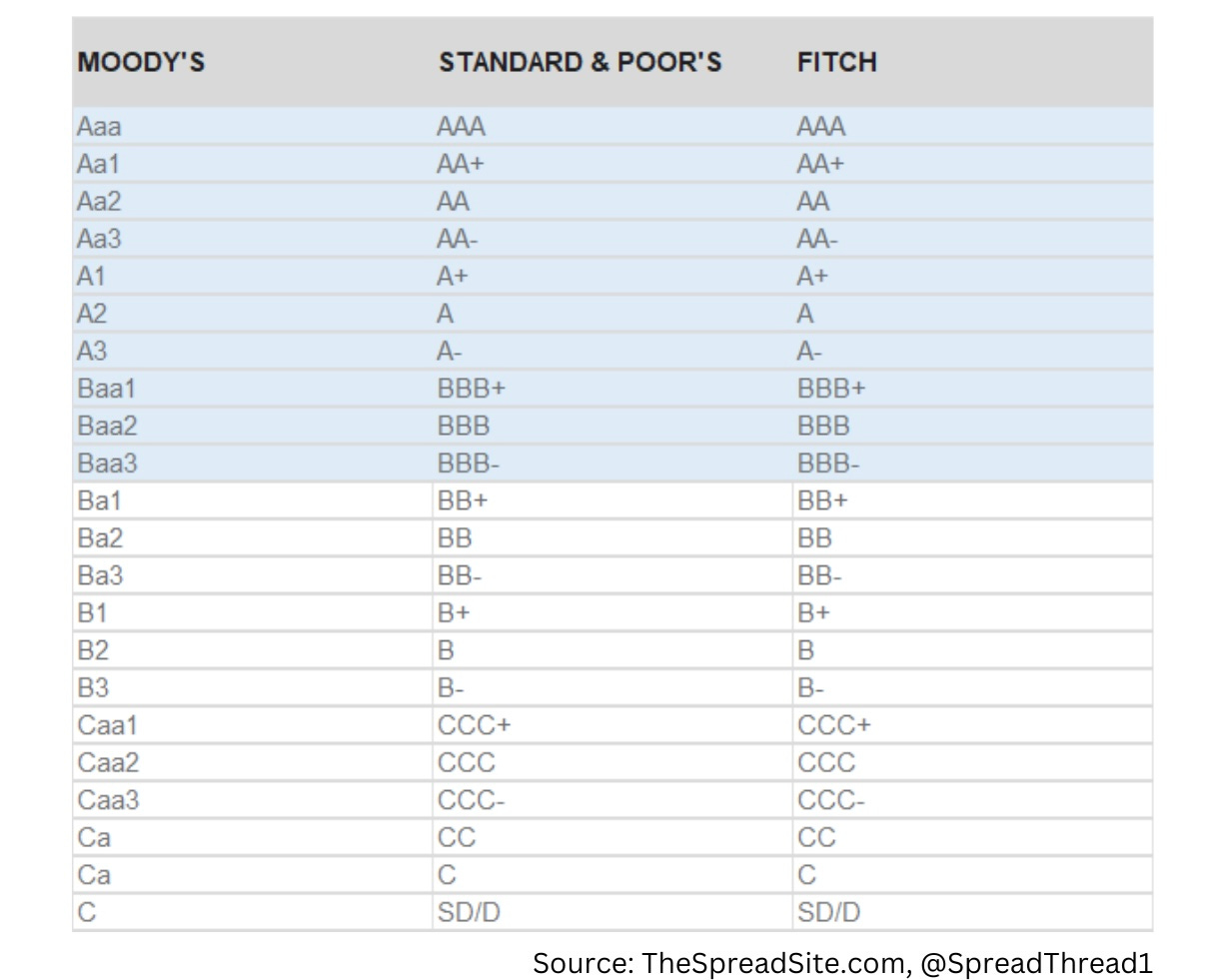

The story of CRAs begins in the early 20th century, a time when Wild West vibes permeated the financial markets. Investors, burned by reckless lending and rampant defaults, craved a beacon of clarity in the midst of the chaos. Thus, agencies like Moody's (established in 1909), Fitch Ratings (established in 1913) and Standard & Poor's (1916) emerged, pioneering the art of assessing financial health and assigning letter grades like creditworthiness report cards.

The ABCs of CRAs:

Fast forward to today, and the CRA landscape is dominated by a "Big Three": Moody's, S&P Global Ratings, and Fitch Ratings. These agencies wield immense power, wielding the ABCs of ratings – from the coveted AAA (highest credit quality) to the dreaded D (default) – that shape investor decisions and, consequently, the fate of corporate bond issuances. Each on of the big three has a slightly different grading system which can be seen

Importance for Corporate Bonds:

So, how exactly do CRAs impact the corporate bond market? Their influence is multifaceted:

Reduced Information Asymmetry: CRAs bridge the information gap between issuers and investors, particularly for non-institutional investors. By meticulously analyzing financial statements, business models, and risk factors, they provide investors with a concise assessment of an issuer's ability to repay debt. This reduces the time and resources investors need to spend on their own due diligence, enabling them to make informed decisions quickly.

Pricing Power: A bond's credit rating directly affects its yield, the return investors receive. Higher-rated bonds offer lower yields, reflecting the perceived reduced risk of default. Conversely, lower-rated bonds carry higher yields, compensating investors for the increased risk. This rating-driven pricing mechanism ensures efficient allocation of capital, directing funds towards financially sound companies.

Market Access: A coveted AAA rating can be the golden ticket for a company seeking to tap the bond market. Investors, particularly large institutions with strict risk guidelines, often prioritize highly-rated bonds. For example public retirement funds, are highly regulated in what the PMs can even consider adding to their fund so highly rated bonds are often all their risk tolerance allows for. Conversely, a downgrade can slam the brakes on fundraising plans, making it difficult or expensive for a company to access capital and in some cases nearly impossible.

Putting it all together:

I’m sure that was a lot of information to take in. If I did not explain a topic enough please comment or reachout via email or Twitter. In the part two of the corp. bond primer we will dive into the different risks associated with investing in corp. bonds. As well a through explanation of yields and yield spreads. A big thank you to

for help with editing this primer! Definitely check out their work.DISCLAIMER: We are not Financial Advisors, and all information presented is for educational purposes ONLY. Financial markets can be highly volatile, so good risk management is a must.

Fantastic piece. It is easy to read, and thanks for breaking a complex subject down.

Great work!!

I'd be keen to know more about the mechanics of buying and selling bonds in secondary markets. I guess the price of it is affected by how interest rates have changed over time, the elapsed time since the bond was issued, how many coupons have been paid and the face value? assuming supply / demand flows are constant to simplify things.

Also stupid question, I assume when you buy a bond you're basically paying for its face value, which could be more or less than when it was first issued based on the previous factors ?

Thanks!!!