ARM's China Problem

ARM's China Problem

A look at the popular chip company

You probably have been hearing about a recent IPO of an European semiconductor company ARM 0.00%↑. I would like to talk about ARM 0.00%↑ and In my its worrying reliance on China.

Let me start with some background first ARM 0.00%↑ has around 90% of its shares owned by Softbank. It is in the business of designing CPU chips and is headquartered in the United Kingdom. The company does not actually build these chips instead they create the architecture for them. ARM 0.00%↑’s main market is the smartphone industry.

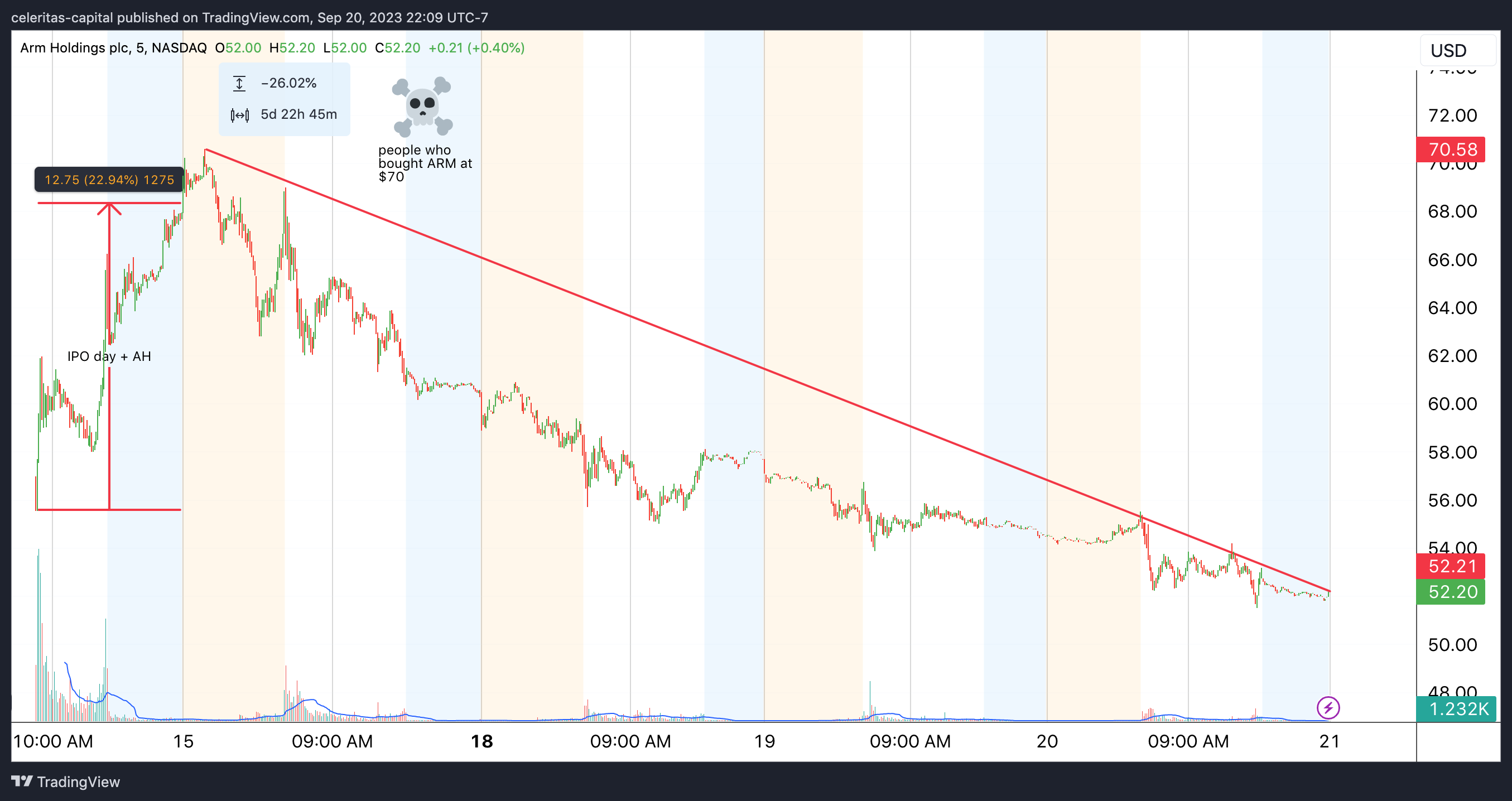

While at first ARM 0.00%↑'s IPO seem to be going well with the shares reaching a high of $70.58. (Figure 1) However, that has been the peak for ARM 0.00%↑ with Figure 1 showing the share price falling back down to its IPO price of $51.

Now I would like to get into some interesting information on the long term viability of ARM 0.00%↑.

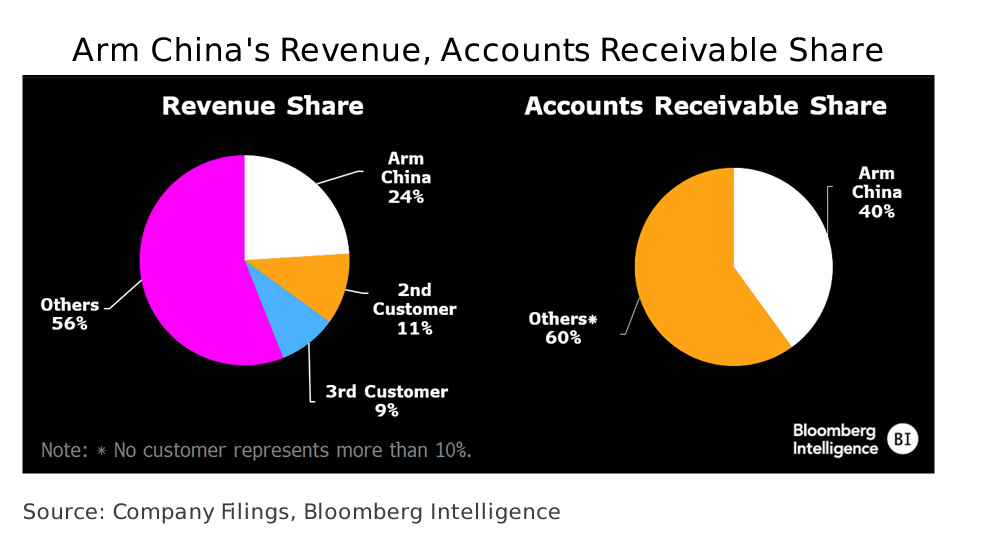

ARM 0.00%↑’s ability to forecast future earnings could be hindered by a problematic relationship with its Chinese subsidiary. ARM China accounted for 40% of ARM 0.00%↑'s accounts receivable and 24% of its total revenue in fiscal year 2023, raising concerns about payment issues. (Figure 2) As we will explore in the next few paragraphs, Arm China has a history of missing payments dates to ARM 0.00%↑. Which should concern any long term investors who own any ARM 0.00%↑ shares. ARM 0.00%↑ 's revenue uptrend may be reversed in fiscal year 2024 due to factors such as declining demand for smartphone chips and economic difficulties in China. Also arguably the most important factor the escalating geopolitical tensions between China and the United States.

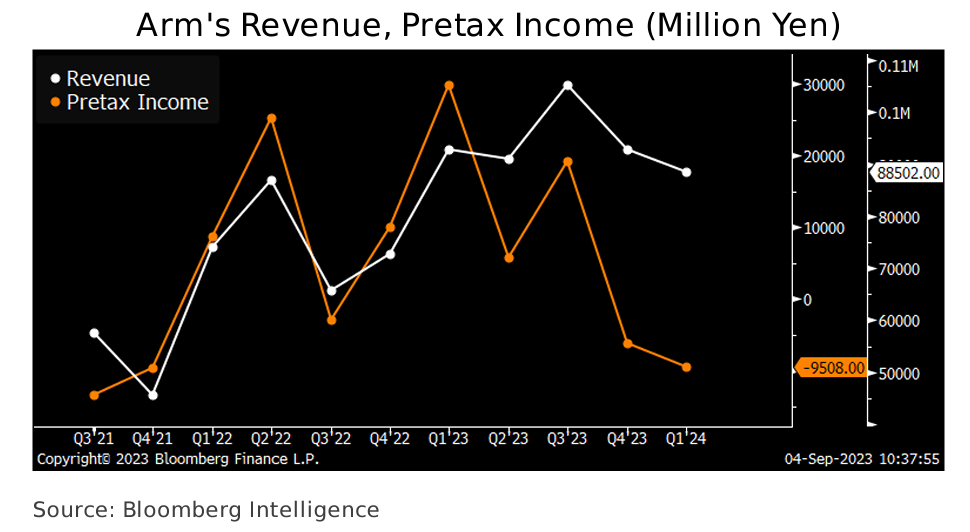

The past payment delays experienced by Arm China (an independent part of the ARM) may signal potential earnings risks for ARM 0.00%↑SoftBank and Arm jointly possess a 48% stake in Arm China. While the rest of the control is vested in various Chinese companies who control the remaining ownership. As I mentioned above Arm China makes a sizeable portion of ARM 0.00%↑’s accounts receivable and its revenue. This was likely thanks to China's large smartphone market. However, Arm China has a historical pattern of delayed payments, as highlighted in Arm's initial public offering (IPO) prospectus. I suspect that this issue has a high likelihood of persisting, indicated by the fact that 40% of Arm's outstanding accounts receivable in fiscal year 2023 originated from Arm China.(Figure 3) Though this figure is a decrease from the 54% recorded in 2022. Additionally, the rising tensions between China and the United States may cause ARM 0.00%↑ problems.

The recent executive directive by US President Joe Biden. Which imposes limitations on investments in semiconductor and microelectronic industries, particularly targeting countries like China, may have adverse consequences on Arm's prospects for sustained profitability. As ARM 0.00%↑ China made up 24% of the firms revenue.

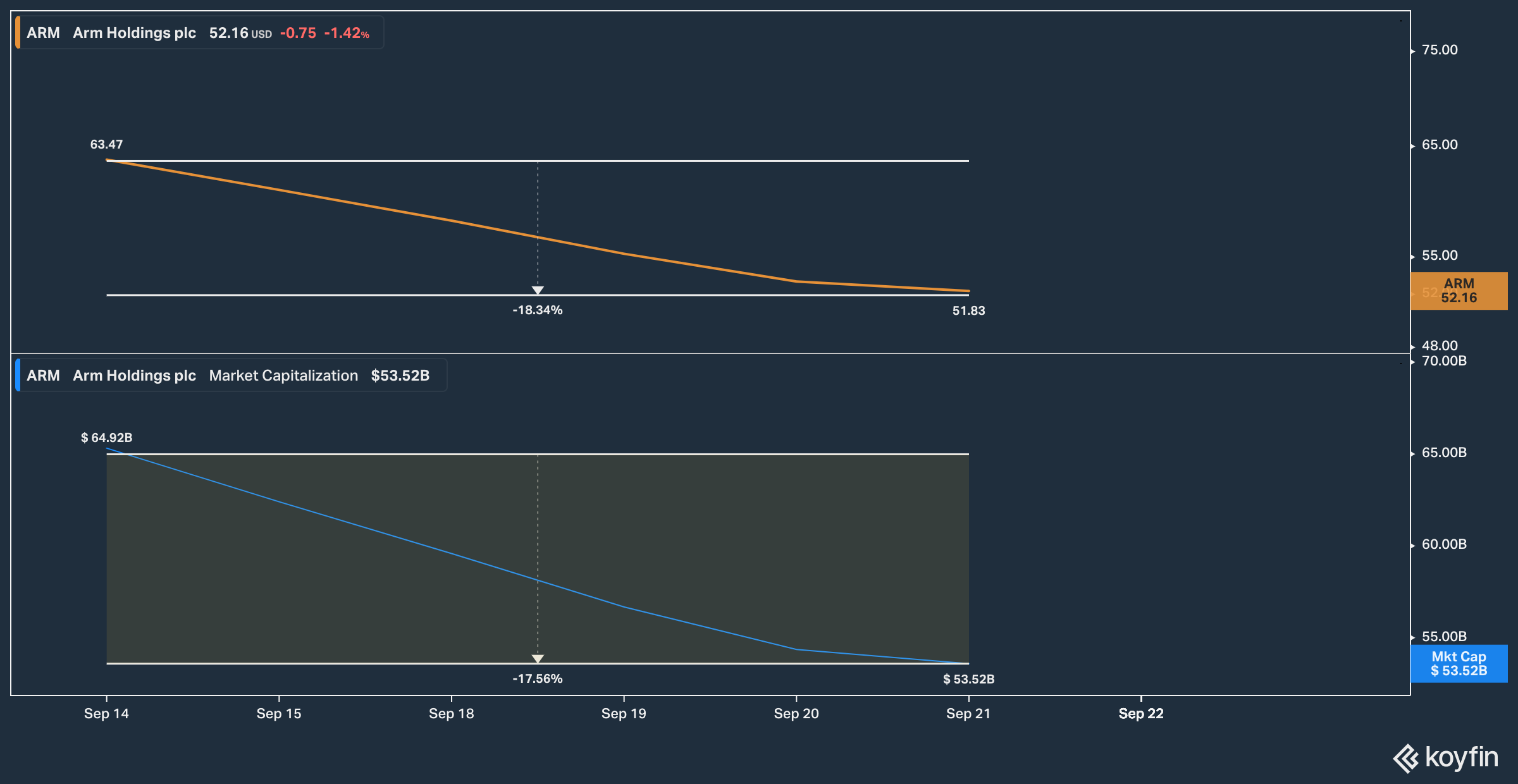

However, these red flags did scare off potential investors as ARM 0.00%↑ IPO with a market cap of $54.5 billion on September 14th. (BBG) Before skyrocketing to a market cap of $64.9 billion and share price of $70 albeit rather briefly. And then falling back to the IPO price of $51ish. (Figure 4)

If you are interested in even more IPO shenanigans I highly recommended

article it is highly detailed and a great read! (Plus he even voices over the article) Make sure you check it out below.

That is all I have for now, I am currently working on my Primer on Modern Monetary Theory. (MMT) As it won the poll on my last post and I want this primer to be a truly great piece of work. I hope you enjoyed today’s post and be on the lookout for the MMT primer I don’t have a set date but hopefully it will be soon. Thank you for the support it is greatly appreciated.

DISCLAIMER: We are not Financial Advisors, and all information presented is for educational purposes ONLY. Financial markets can be highly volatile, so good risk management is a must.